: ₹20L Setup, EPR & 10-Step Plan")

1. What Does an E-Waste Recycling Business Do?

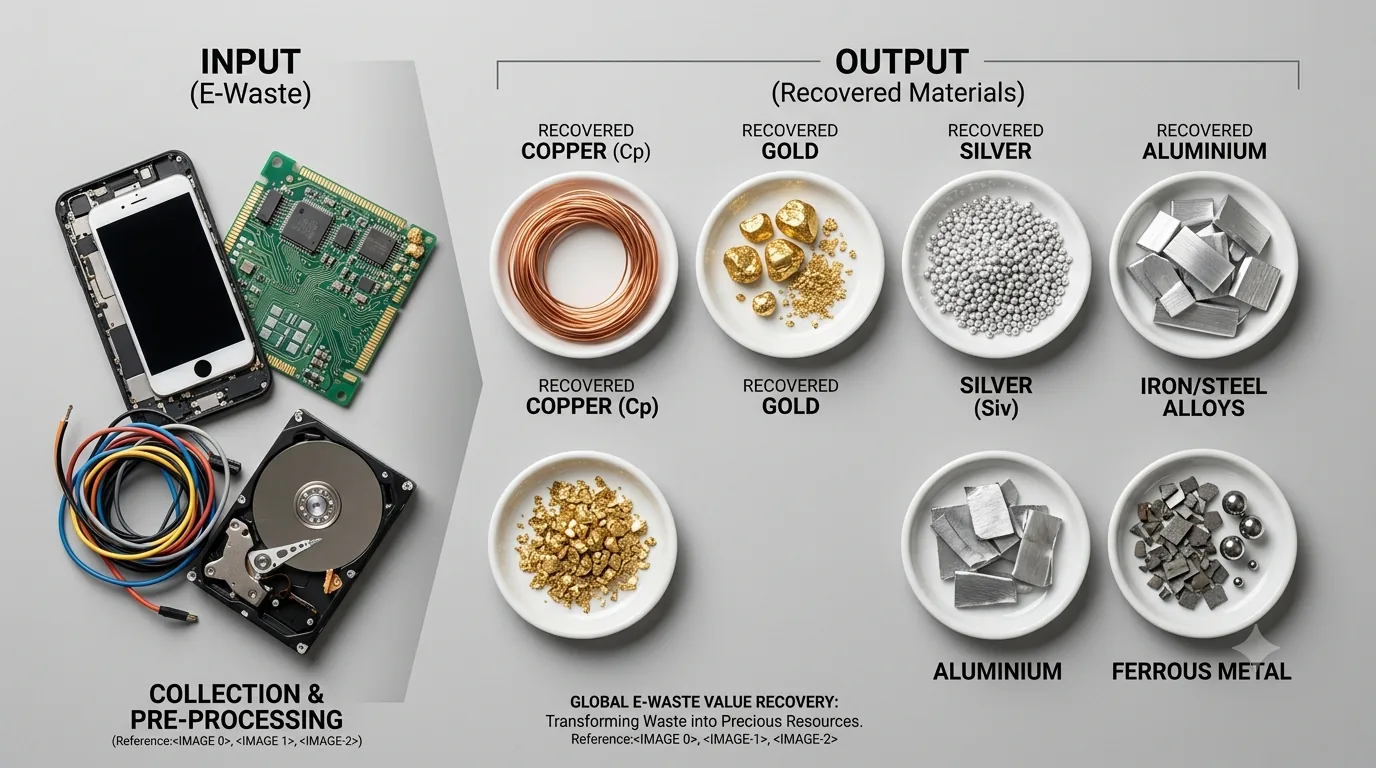

An e-waste recycling business collects used electrical and electronic equipment and recovers raw materials from it. Electronic and electrical equipment contains various metals. E-waste recycling processes this equipment to recover metals, mainly iron or steel alloys, copper, gold, aluminium, and silver.[1] For example, one tonne of mobile phone PCBs contains more gold than a tonne of high-grade mined ore.[2]

Links you might be interested in

E-waste volumes are rising as more electronic and electrical appliances are used. The global e-waste recycling market may reach $145 billion by 2030, with a CAGR of 13.2%. About 347 million metric tonnes of e-waste remain unrecycled worldwide, and annual generation could reach 82 million tonnes by 2030. In 2022, global e-waste contained about $91 billion in raw materials, but only $19 billion was recovered. Most of the value is still lost.[3] To judge the business, you need to understand the technical and commercial factors that decide outcomes.

2. E-Waste Market Size and Industry Outlook in India (2026)

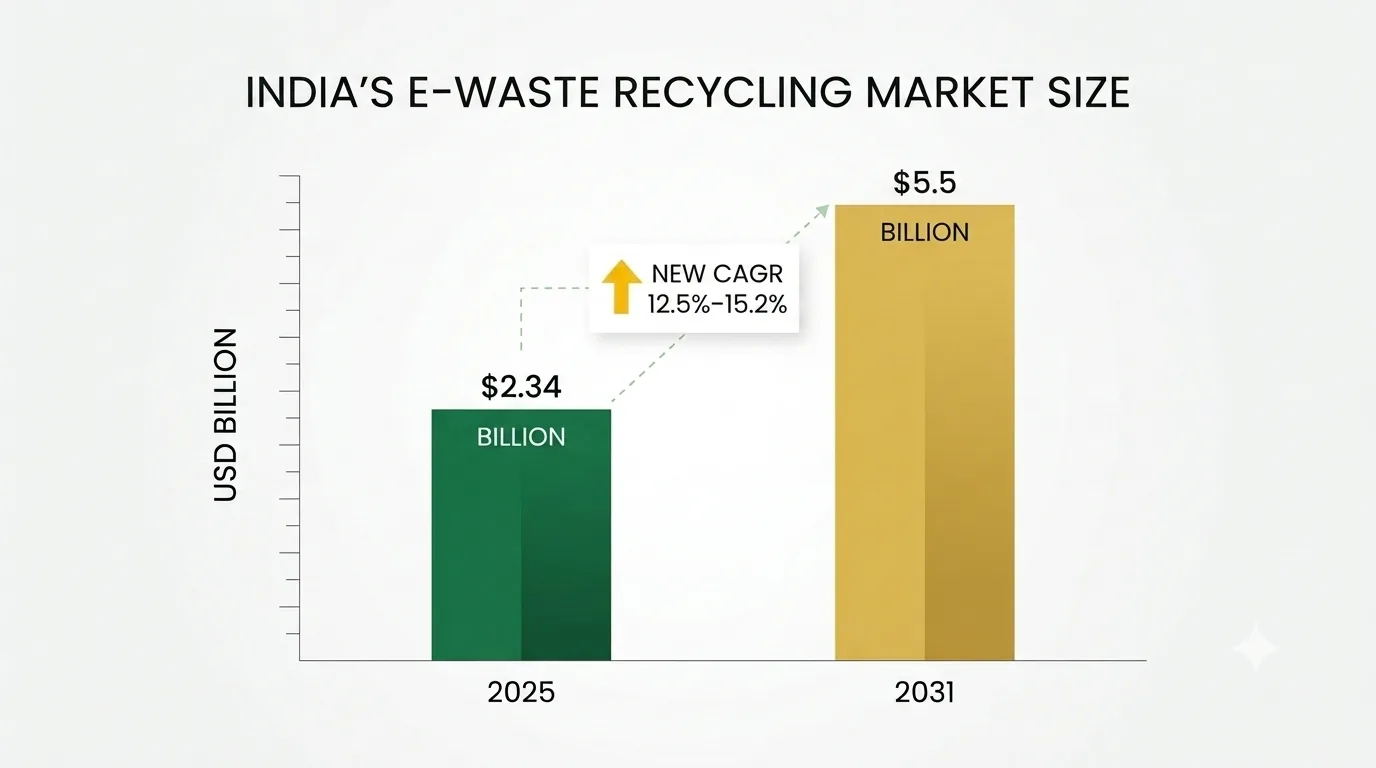

Three trends shape the Indian e-waste market: more electronic use, shorter device lifespans, and stricter producer compliance rules. Formal-sector recycling capacity is still much lower than the e-waste generated.[4] India’s e-waste management and recycling market was valued at $1.88–2.8 billion in 2025. By 2031, it is projected to reach $2.87–5.5 billion, with a CAGR of 7.3- 10.1%.

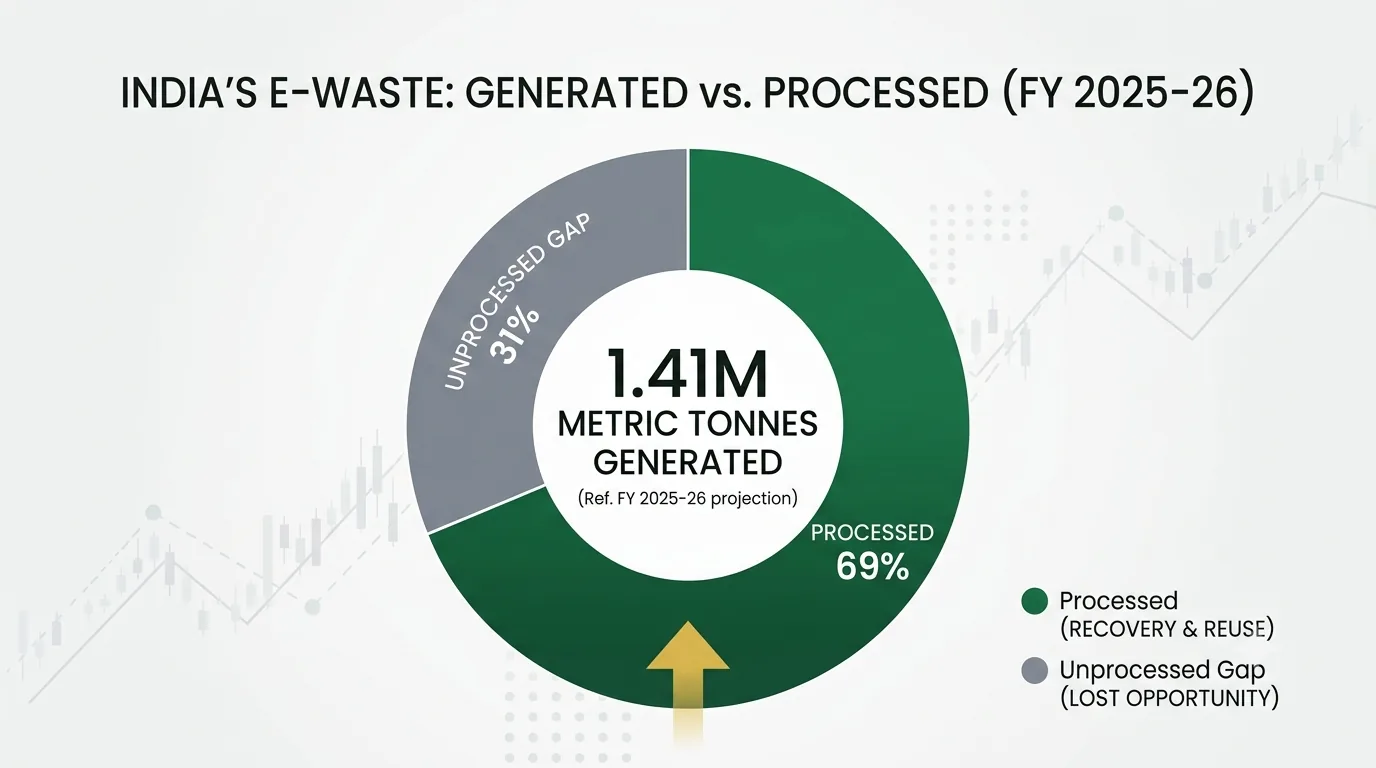

In FY 2025-26, India generated 1,414,645 metric tonnes (MT) of e-waste. Of this, 979,080 MT was processed through registered channels. The gap between generated and processed waste shows the need for more recycling.

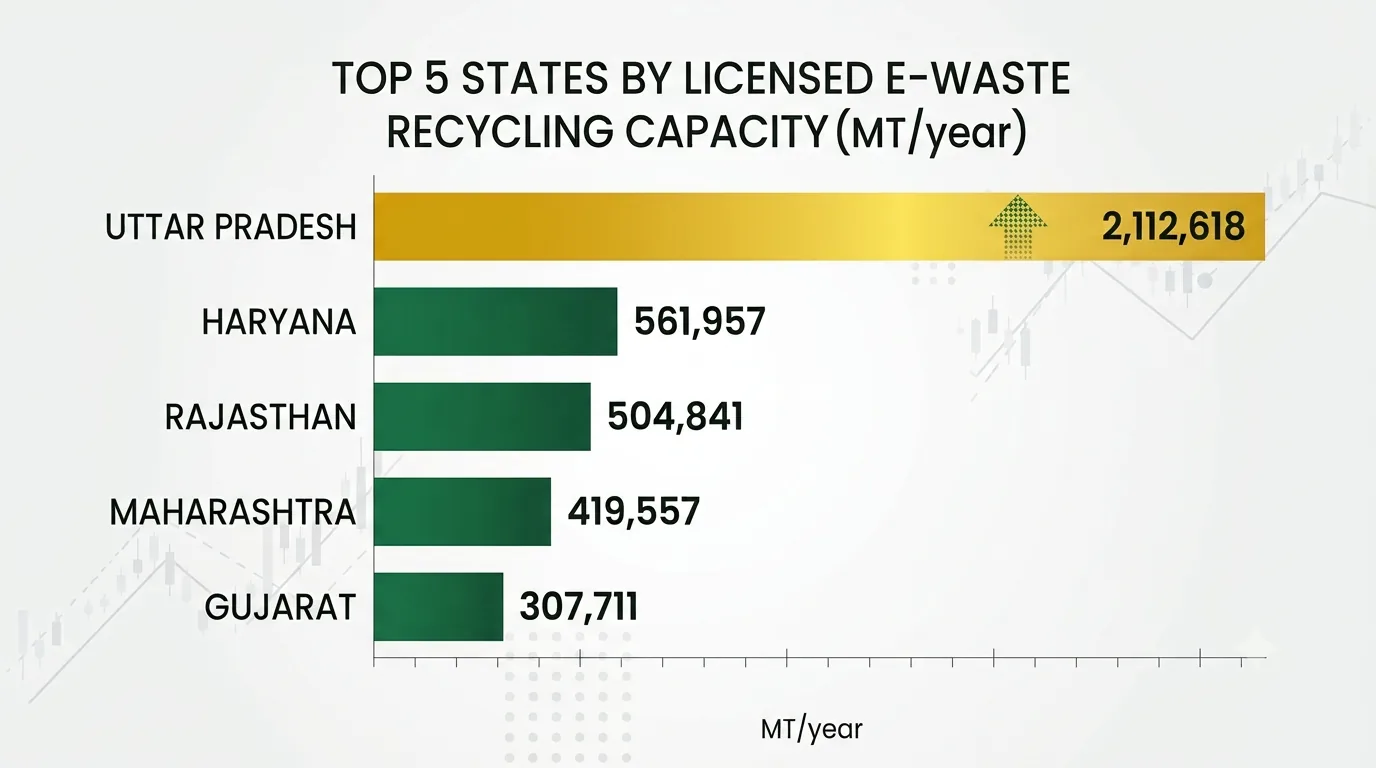

India’s recycling rate increased from 9.8% to 43.4% between 2017-18 and 2023-24.[5] This growth shows e-waste recycling is now a viable business.371 recyclers are registered on the EPR PortalEPR PortalOnline regulatory platform for tracking producer responsibility compliance and waste recycling targets in India. in India. The numbers for producers, manufacturers, and refurbishers are 11,930, 136, and 144, respectively. The gap between recyclers and producers suggests a need for more recyclers in the market. The top 5 states with maximum Licensed capacity (MT/yr) are shown below –

| State | Recyclers | Licensed capacity (MT/yr) | Avg per recycler | % of national |

|---|---|---|---|---|

| Uttar Pradesh | 108 | 2,112,618 | 19,561 | 44.8% |

| Haryana | 39 | 561,957 | 14,409 | 11.9% |

| Rajasthan | 17 | 504,841 | 29,697 | 10.7% |

| Maharashtra | 65 | 419,557 | 6,455 | 8.9% |

| Gujarat | 35 | 307,711 | 8,792 | 6.5% |

Most recycling operations are in a few states. This means large amounts of e-waste are moved over long distances. If you set up in other states, you can fill this gap. E-waste recycling is growing quickly because waste volumes are rising, there are not enough recyclers, and recovered metals have real value. These are the main reasons the business works. The market has real challenges. Informal-sector competition reduces margins on low-value plastics and ferrous metalsFerrous MetalsIron-based metals — mild steel, stainless steel and cast iron — that are magnetic and form the heaviest recyclable fraction of e-waste. Separated with magnets and sold to steel mills.. Logistics costs are high, and working capital cycles are long. [6] You can find detailed industry data on the Indian e-waste sector, including TAM modelling, sector shares, and projected growth rates through 2030, on Adhara Viveka. Use this to check your market assumptions before you invest.

Ready to validate your e-waste business idea?

Access detailed sector overviews, competitor analysis, and growth forecasts to make informed decisions before you launch.

3. Regulatory Policy Drivers Accelerating Sector Growth

Government policies have increased e-waste recycling activity[7]. The two main drivers are EPR targets set by the Central Pollution Control Board and government support through subsidies and grants[8].

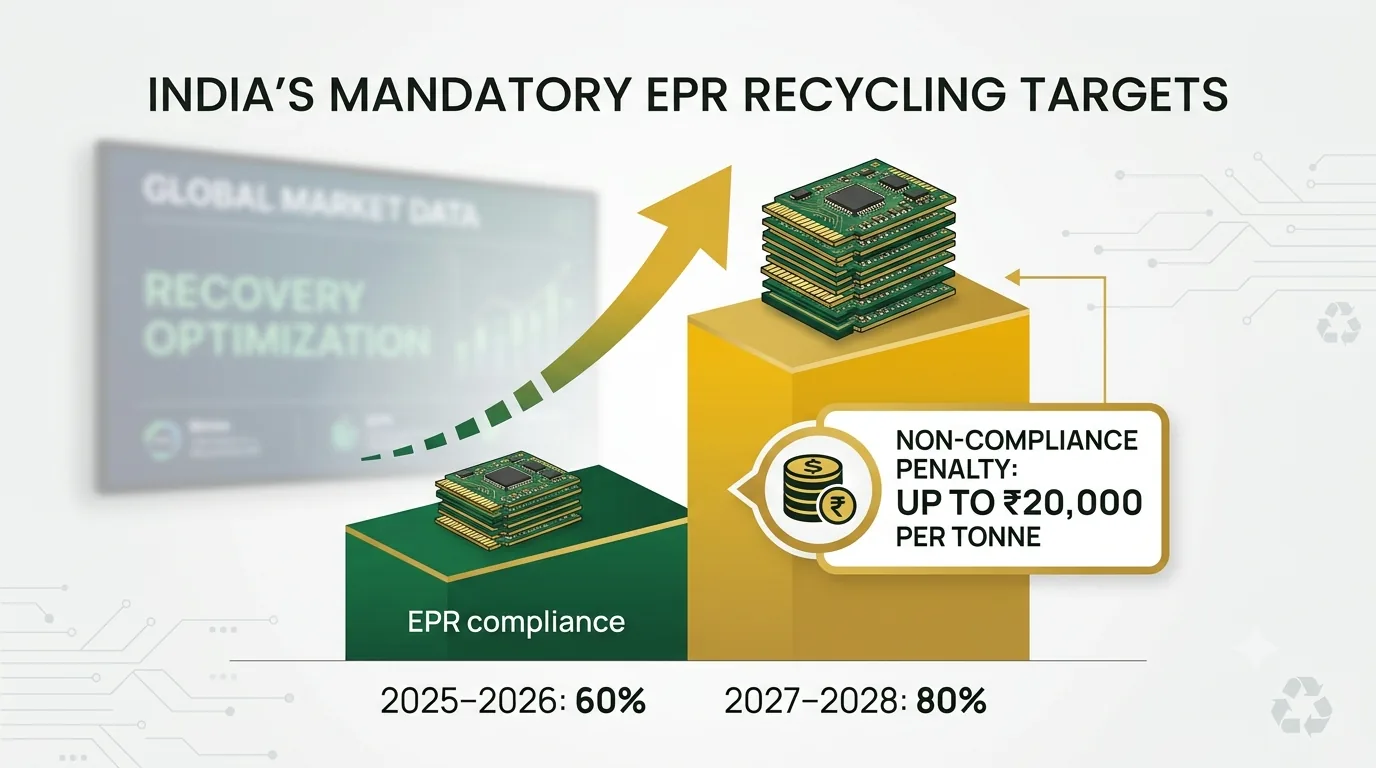

3.1 The 60% Mandatory Extended Producer Responsibility (EPR) Framework

Under the E-Waste (Management) Rules, 2022, tech manufacturers and importers face a legally mandated EPR recycling target of 60% for the 2025–2026 cycle, escalating to 80% by 2027–2028, with non-compliance risking heavy financial penalties of up to ₹20,000 per ton.

EPR (Extended Producer Responsibility) plays a crucial role. In FY 2023-24, the total producer recycling obligation was about 266,616 MT, against which 261,220 MT was achieved, and 262,188 MT of EPR credit was generated. (E-Waste Management Rules, 2022, 2022) Targets for specific metals are given below –

| Material | FY 2023-24 recycling target |

|---|---|

| Iron | 218,629 MT |

| Aluminium | 29,092 MT |

| Copper | 18,895 MT |

| Gold | 51.6 kg |

EPR targets are large enough that EPR credits are a real source of revenue for recyclers, not just a CSR activity[9].

3.2 National Critical Mineral Mission (NCMM):

Launched on October 2, 2025, the NCMM’s ₹1,500-crore incentive scheme targets the development of e-waste and lithium-ion battery recycling infrastructure to secure a localised, reliable supply of critical domestic minerals such as lithium and cobalt[10].

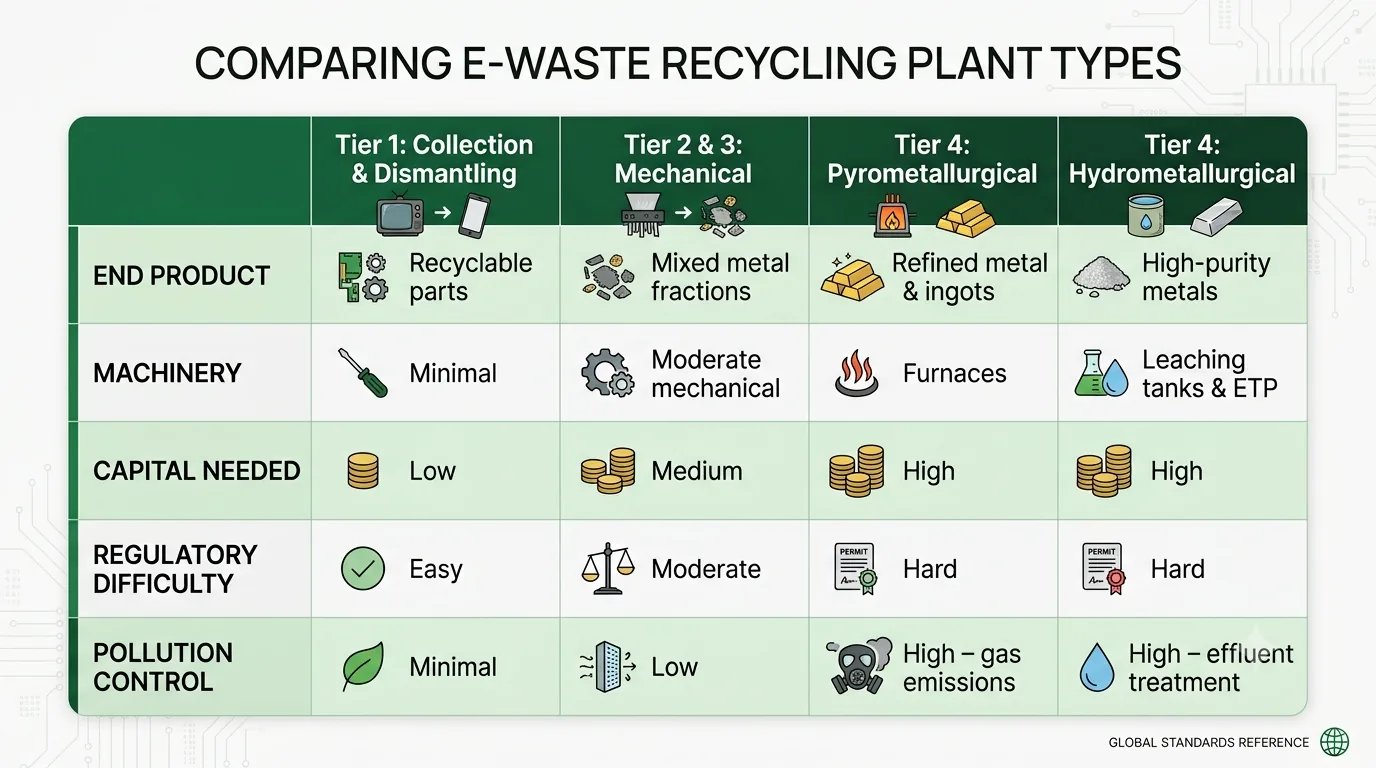

4. Classifying E-Waste Recycling Plant Typologies

E-waste recycling plants come in several forms. You need to understand the types because this will decide your process flowProcess FlowThe sequence of operational steps that transform waste or raw materials into finished products., feedstock, end product, regulatory requirements, plant location, and layout. Below are the main types of plants you can set up.

4.1 Collection and Dismantling Facilities (Tier 1)

Collection and dismantlingDismantlingThe manual or semi-automated teardown of end-of-life electronics into separate fractions — circuit boards, metals, plastics and hazardous parts — so each can be recovered or disposed of correctly. plants collect electronic scrap and break it down into smaller parts. These need minimal machinery and are easier to get approvals for. You do not recover individual metals here; instead, you sell recyclable parts to other plants for further processing.

4.2 Mechanical Recycling Plants (Tier 2 and 3)

Mechanical recyclingMechanical recyclingThe process of sorting, washing, shredding, and melt-extruding waste plastic into recycled pellets without breaking the polymer’s chemical structure — the dominant recycling method for post-consumer plastic in India. plants use only mechanical processes to recover metals. Their machinery setup is more complex than a dismantling plant but does not use furnaces or leaching tanks, as in pyrometallurgical or hydrometallurgical setups. The end products are mixed fractions: ferrous, non-ferrous, and a concentrated precious-metal-bearing fraction[11]. Depending on your setup, you may get all three or just one or two. Regulatory approvals for these plants are easier than for pyrometallurgical or hydrometallurgical plants, because the processes are only mechanical.

4.3 Advanced Refining and Smelting Facilities (Tier 4)

- Pyrometallurgical Recycling Plants:

In pyrometallurgical plants, metal mixtures are heated to high temperatures in furnaces to remove impurities and produce refined metal or ingotsIngotsStandardized metal or material form produced by casting molten scrap into molds for recycling and reprocessing. [12]. Most setups use pyrometallurgy as an extension of mechanical recycling. The mixed fraction from mechanical plants is further processed to produce refined metal or ingots. Heating metals at high temperatures releases toxic gases [13]. You need more pollution-control systemsPollution-Control SystemsSystems that treat and control emissions, effluents, and waste from industrial facilities to comply with environmental standards. for this process, and approvals are harder to get.

- Hydrometallurgical Recycling Plants:

Hydrometallurgical plants use chemical and aqueous solutions to leach, separate, and recover high-purity metalsPurity MetalsThe concentration and degree of separation of a target metal from impurities in recovered waste material.. Hydrometallurgy is common for precious-metal recovery and high-purity output [14]. Like pyrometallurgical setups, these are usually extensions of mechanical setups for further purification. Hydrometallurgical plants use toxic chemicals, so you need an on-site ETP [15] (Effluent Treatment PlantEffluent Treatment PlantA facility that treats industrial wastewater (effluent) to remove pollutants before discharge — its design and flow diagram are part of the project report submitted with consent applications.). Approvals are also harder to get. These are not four separate business types. They are process extensions you can add as needed. You can start with collection and dismantling or a mechanical setup, which need less capital and are easier to approve. Once you have a base, you can add pyro or hydro setups. Each step lets you recover metals in purer form and capture more value, but costs, complexity, and regulatory requirements all go up.

5. Feedstock Understanding and Ecosystem Roles

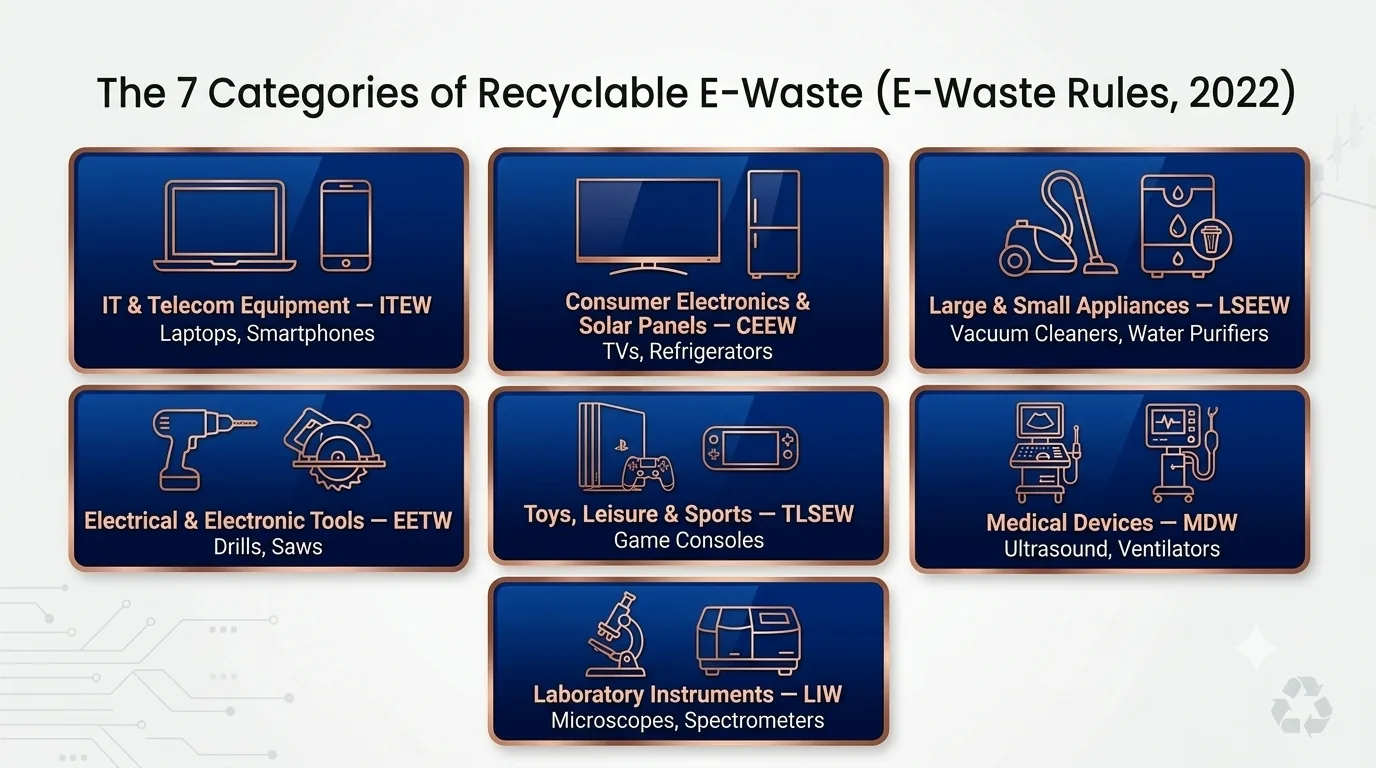

There are over 100 types of electrical and electronic equipment, grouped into 7 categories, that can be recycled [16]. You will not recycle them all. You need to pick the right feedstockFeedstockRaw materials fed into the anaerobic digestion process, typically organic waste streams from industrial or agricultural sources, which means understanding the role feedstock plays in the e-waste recycling ecosystem. Under the E-Waste (Management) Rules, 2022, feedstock is now divided into seven categories, each having its own item code [17]. I am sharing the list of these categories and what they cover below –

| Sl. No. | Item Code | Official Category Name | Key Items Covered |

|---|---|---|---|

| 1 | ITEW1 to ITEW27 | Information Technology and Telecommunication Equipment | Centralized data processing systems, Mainframes, Minicomputers, Laptops, Notebooks, Smartphones, Feature phones, Routers, GPS devices, Tablets, and Scanners. |

| 2 | CEEW1 to CEEW19 | Consumer Electrical and Electronics and Photovoltaic Panels | Television sets (CRT/LCD/LED), Refrigerator units, Air Conditioners, Washing machines, Radio sets, and Solar Photo-Voltaic Modules/Panels/Cells. |

| 3 | LSEEW1 to LSEEW34 | Large and Small Electrical and Electronic Equipment | Large cooling appliances, Vacuum cleaners, Water purifiers, Luminaires, Heating appliances, Toasters, and Electronic clocks. |

| 4 | EETW1 to EETW8 | Electrical and Electronic Tools (with the exception of large-scale stationary industrial tools) | Drills, Saws, Sewing machines, Grinders, and tools for milling, sanding, turning, or folding wood and metal. |

| 5 | TLSEW1 to TLSEW6 | Toys, Leisure, and Sports Equipment | Video game consoles, Handheld video game devices, Electric trains/racing car sets, and sports equipment with electric components. |

| 6 | MDW1 to MDW10 | Medical Devices (with the exception of all implanted and infected products) | Radiotherapy equipment, Cardiology monitors, Ultrasound scanners, Ventilators, and Laboratory analyzers. |

| 7 | LIW1 to LIW2 | Laboratory Instruments | Chromatographs, Spectrometers, Microscopes, Autoclaves, and specialized electronic measuring, weighing, or testing laboratory rigs. |

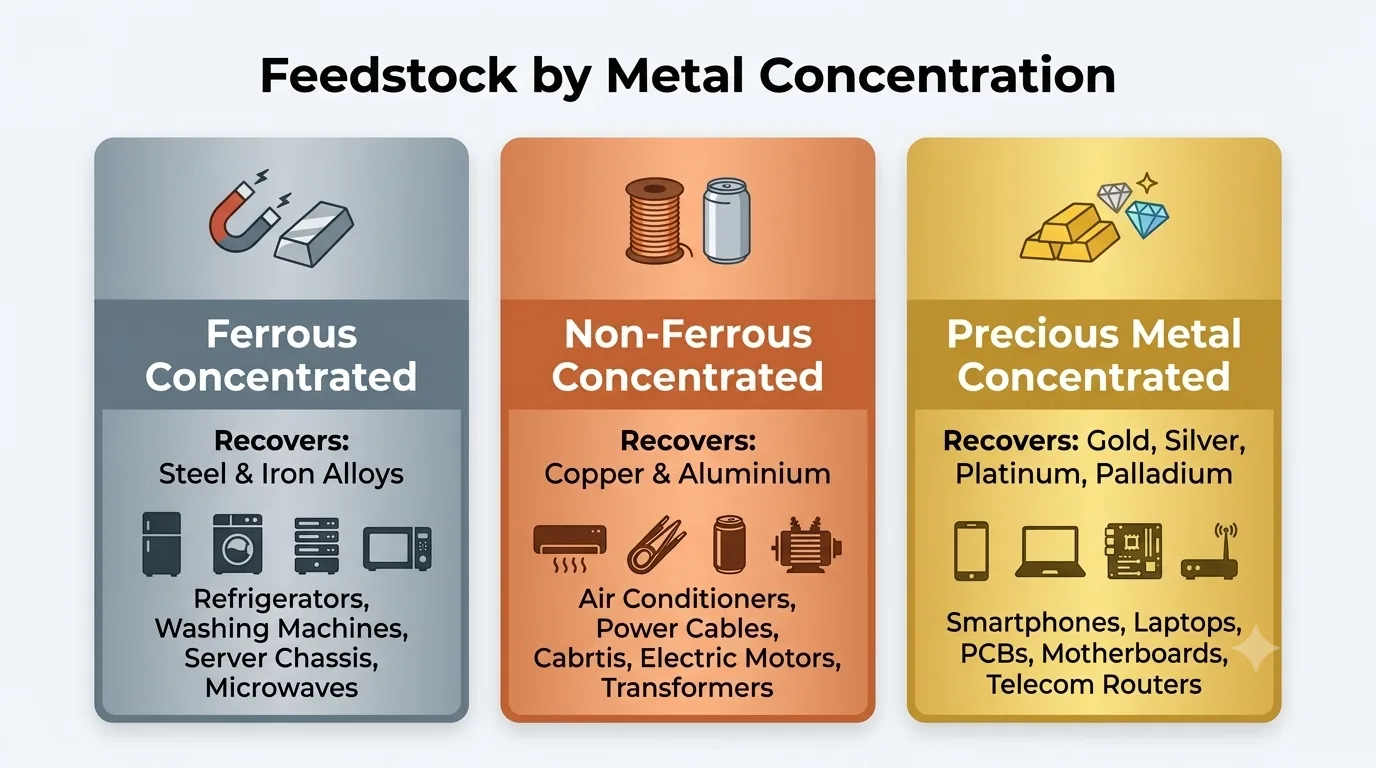

5.1 Feedstock categorisation based on metal concentration

Not all feedstocks have the same metal concentration. As a recycler, you can group them into three types based on which metal is most concentrated [18]:

- Ferrous Metal Concentration FeedstockFerrous Metal Concentration FeedstockIron-rich material processed to concentrate non-ferrous metals for downstream recovery. – Have a high concentration of Iron and Steel Alloys.

- Non-Ferrous Metal Concentration FeedstockNon-Ferrous Metal Concentration FeedstockProcessed material enriched with non-ferrous metals from waste, ready for smelting or refining. – Have a high concentration of Copper and Aluminium.

- Precious Metal Concentration FeedstockPrecious Metal Concentration FeedstockWaste materials with economically recoverable concentrations of precious metals processed for extraction and refining. – Has a high concentration of Precious Metals, such as gold and silver [19].

Below is a table with details on different metal-concentration-based feedstock categories and the common e-wastes under them –

| Material Profile | Key Recoverable Elements | Common Feedstock Items |

|---|---|---|

| Ferrous Metal Concentrated | Steel and Iron Alloys | Refrigerators, Freezers, Washing Machines, Clothes Dryers, Server Chassis, Mainframe Racks, Microwaves, Large Cooling Appliances |

| Non-Ferrous Metal Concentrated | Copper and Aluminium | Air Conditioners (Indoor/Outdoor units), Bulk Power Cables, Electric Motors, Industrial Drills, Saws, Grinders, Transformers, Geysers, Voltage Stabilizers |

| Precious Metal Concentrated | Gold, Silver, Platinum and Palladium | Smartphones, Laptops, Notebooks, Desktop PCBs, Motherboards, Server Blades, Telecom Switching Routers, Smart TVs, Medical Ultrasound Analyzer Boards, X-Ray Logic Boards |

Your feedstock will also contain non-recyclable hazardous parts. You will need to send these to a TSDF (Treatment, Storage, and Disposal Facility)TSDF (Treatment, Storage, and Disposal Facility)A regulated facility for managing hazardous waste through treatment, storage, or safe disposal.. Besides recoverable metals and non-recyclable hazardous parts, your feedstock will also have glass, batteries, plastics, and other components. You will not recycle these yourself. After dismantling, you collect and sell them to specialist recyclers. This is an extra source of revenue. Plastics with Brominated Flame RetardantsBrominated Flame RetardantsBrominated Flame Retardant — toxic flame retardants used in plastic casings of electronics; their presence determines whether the recovered plastic is recyclable or must be disposed of. (BFRs) cannot be sold to ordinary plastic recyclers.

5.2 Feedstock Sourcing Infrastructure

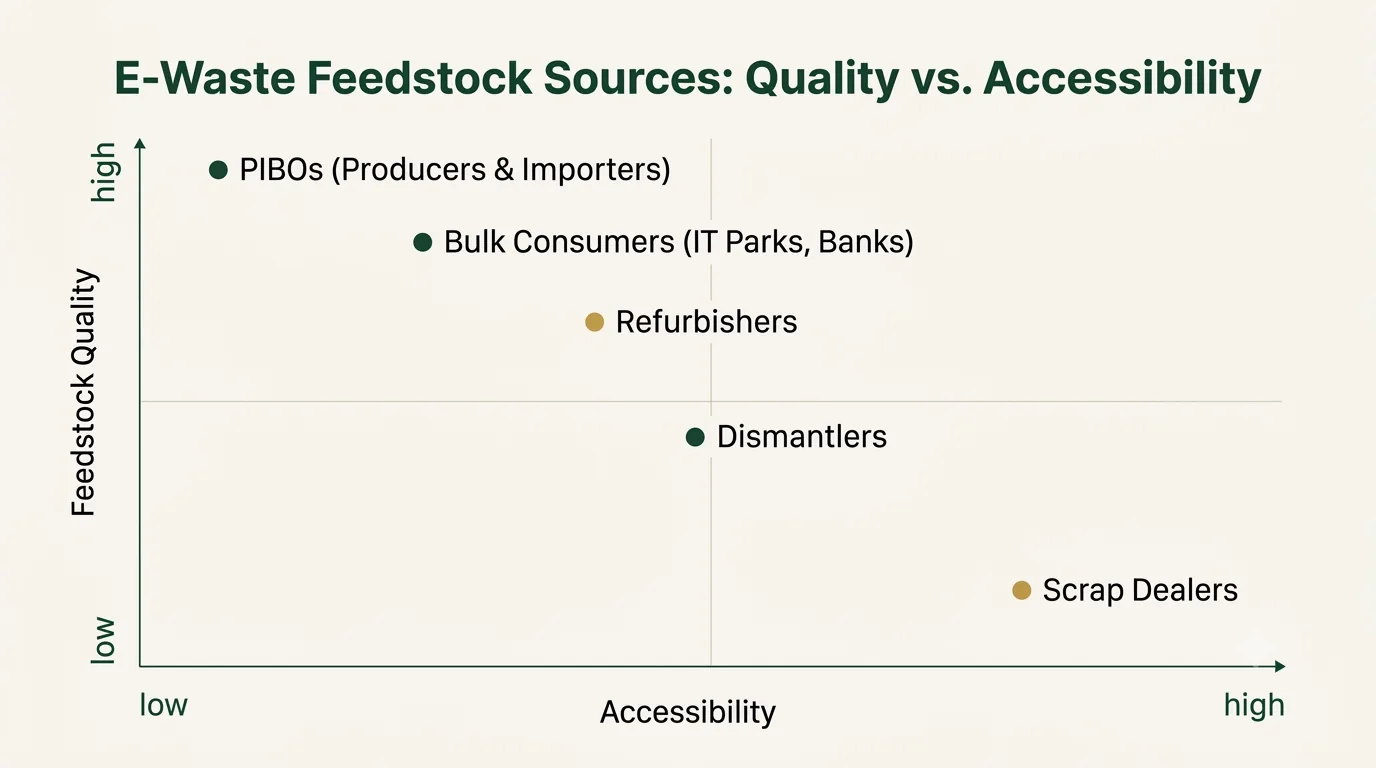

To get your feedstock, you will need to know where to get it. Below are your potential sources of feedstock –

- Producers, Importers and Brand Owners (PIBOsPIBOsEntities responsible for managing end-of-life waste from their products under EPR regulations.) – These are entities that introduce electronic and electrical items in the country. If an item does not pass a quality test, they are happy to give it to recyclers.

- Bulk Consumers – Entities that purchase electronic items in bulk. These are your IT Parks, banking chains, etc.

- Scrap Dealers – Scrap dealers will be your bulk source of electronic scrap. They do door-to-door collection through their network.

- Refurbishers repair electronic devices and put them back into circulation. Many times they have parts which are non-functional and sell them to recyclers.

- Dismantlers – Dismantlers collect electrical and electronic equipment and sell the dismantled parts to recyclers.

Feedstock quality and availability vary by source. PIBOs and bulk consumers offer the best feedstock, but supply is limited, and competition is high. Refurbishers and dismantlers provide better quality than scrap dealers. Scrap dealers have the lowest-quality feedstock but are the most accessible [20].

6. Licenses, EPR and Regulatory Compliance for E-waste Recyclers in India

Regulatory approvals for E-waste recycling plants are governed by different government agencies. It is important that you understand which regulations apply to you and who governs them. Below, I have detailed the various regulations that will apply during your plant setup.

6.1 Licenses and certifications you will need

What licenses and EPR rules apply to you?

Master e-waste regulations, CTE/CTO requirements, and compliance essentials that drive sector growth.

Business Formation documents: You will need to register your company on the MCA Portal. In addition, you will need –

- PAN (Permanent Account Number) – You will need this to file income tax returns on profits from the sale of recovered metals and EPR CertificatesEPR CertificatesCertificates issued to producers as proof of meeting Extended Producer Responsibility recycling obligations..

- TAN (Tax Deduction and Collection Account Number) – Once your plant starts making payments, tax will be deducted at source (TDS) and collected at source (TCS). This is where TAN becomes relevant. When you purchase e-waste or metal scrap, you will be deducting TDS, and you will be collecting (TCS) on sale of recovered metal. Note that these TDS and TCS are applicable above certain turnover thresholds.

- GST (Goods and Services Tax) registration – GST is an indirect tax on the supply of goods and services in India. GST allows input tax credit, which means the GST that you will pay on your purchases is adjusted against the GST you charge on sales. This brings your cost down. This is particularly beneficial, as you will be investing heavily in machinery and equipment such as shreddersShreddersMechanical equipment that breaks down waste into smaller pieces for downstream recycling processes., separators, and classifiers.

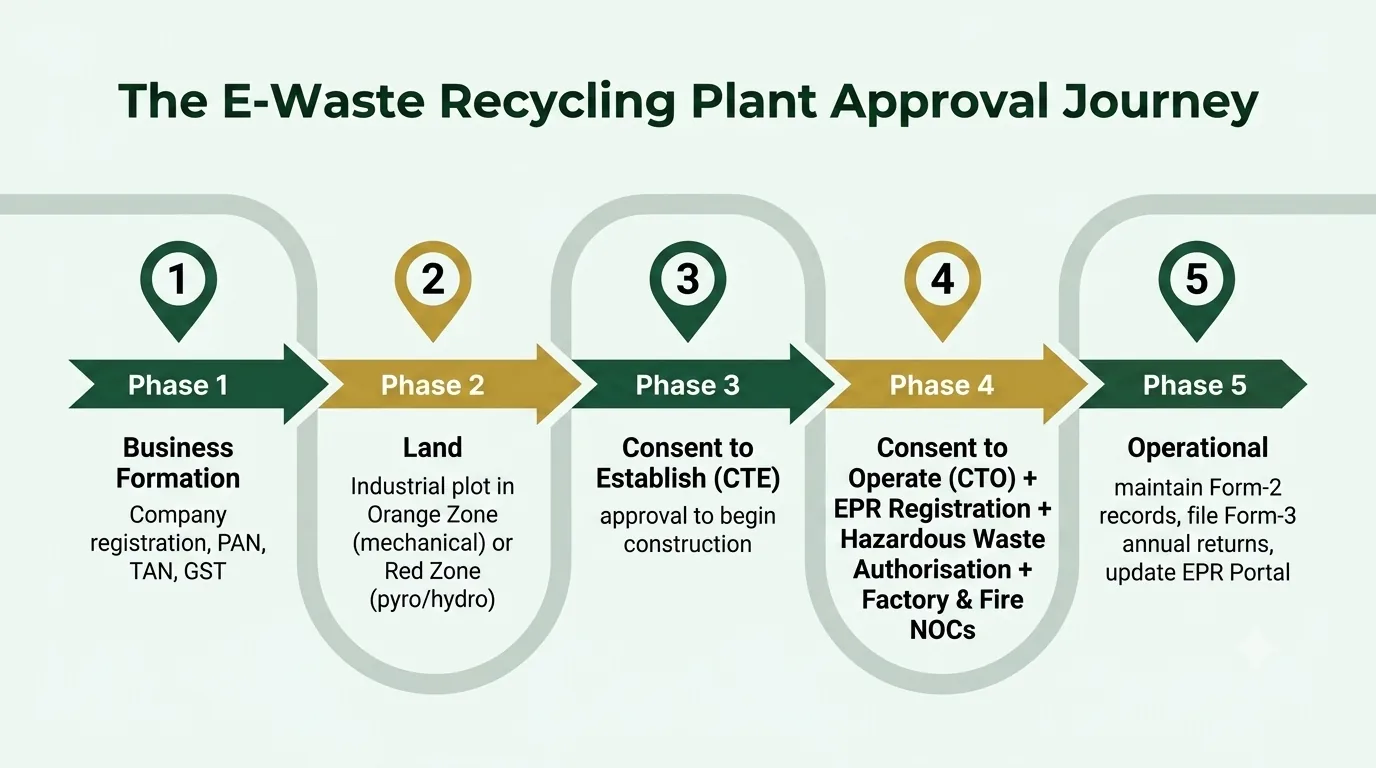

Land Documentation: You will need to procure land with proper documentation for the plant setup. You will require Industrial Land in the Orange or Red ZoneRed ZoneThe highest pollution-risk industrial classification requiring strict environmental controls and regulatory compliance., depending on the plant setup and variant [21]. Typically, a purely mechanical recycling plant can use the Orange ZoneOrange ZoneModerate pollution industrial classification requiring environmental permits and compliance monitoring., whereas Pyrometallurgical or Hydrometallurgical setups require the Red Zone [22]. Environmental Pre-Construction Clearances: You will need a Consent to Establish (CTE) before starting the construction. Environmental Clearance under the EIA Notification 2006EIA Notification 2006S.O. 1533 dated 14th September 2006 — the central rule that requires prior Environmental Clearance for listed project categories, defines screening / scoping / public consultation / appraisal stages, and lists exemptions. is generally not required for e-waste mechanical recycling plants; however, pyrometallurgical and hydrometallurgical setups require an explicit prior Environmental Clearance from either the State (SEIAA) or the Central Ministry (MoEF&CC) [23]. Pre-commissioning: Before you can operate the plant, and once the setup is ready for inspection, you will need the following clearances and documents:

- Consent to Operate (CTO)Consent To Operate (CTO)Mandatory environmental clearance required for industrial operations to legally commence and continue processing. from the State Pollution Control Board.

- Central CPCB PortalCPCB PortalDigital platform managed by CPCB for waste management registration, environmental clearance, and compliance reporting. Recycler Registration on the EPR portal, which tracks your procurement, recycling and certificate generation

- Hazardous Waste Authorisation (Form 1)Hazardous Waste Authorisation (Form 1)Regulatory authorisation required to legally handle hazardous waste in India. coupled with a mandatory signed TSDF (Treatment, Storage, and Disposal Facility) Agreement for toxic residue disposal.

- Proof of specialised infrastructure compliance (Impermeable acid-resistant flooringImpermeable Acid-Resistant FlooringChemical-resistant flooring that prevents acid and corrosive liquid penetration in industrial settings. and Acoustic enclosures for shredders) [24].

- Factory Licence under the Factories Act, 1948Factories Act, 1948India’s primary occupational health and safety law for manufacturing units; defines licensing, working hours, hazardous-process duties, and welfare requirements for factory occupiers..

- Electrical Safety NOC and Fire Safety NOC.

Post-Operational

- Maintain records of e-waste handled in Form-2Form-2CPCB authorization application required for waste recycling and processing facility operations in India. and prepare logbooks for the operations.

- File Annual returns in Form 3Form 3Authorization certificate required under Indian e-waste rules for legal operation of collection, dismantling, recycling, or refurbishment activities.

- Update all information in the EPR Portal.

6.2 Documents needed for CTE (Consent To Establish) and CTO (Consent To Operate):

CTE and CTO are the most important consents you will need for your plant setup. CTE is needed so you can start setting up your plant. After this, only civil works and machinery procurement will be done; this will follow. CTO is the consent needed to start operating the plant. You apply for this once all phases of plant setup are complete and you are ready to operate. Below, I am sharing the documents needed for these – Consent To Establish (CTE)Consent To Establish (CTE)Mandatory environmental clearance required before construction of industrial facilities in India.

- Land Possession Proof – You will need to provide a registered sale deed or a long-term registered Lease Deed. It is important that the document explicitly states that the land can be used for industrial purposes and the land’s zone.

- Corporate Identity – You will need to provide a Certificate of Incorporation (from the Registrar of Companies), Partnership Deed, or Proprietorship Registration, along with the Company’s PAN Card.

- Industry Registration – Your Micro, Small, and Medium Enterprises (MSME) registration or a Directorate of Industries acknowledgement.

- Detailed Project Report (DPR)Detailed Project Report (DPR)A comprehensive technical and financial document required to obtain regulatory approvals and financing for waste-to-value projects in India. – a document that provides information on the nature of the plant setup, hazardous materials, your proposed capital investment, production capacity and air pollution mitigation protocols, and other specific details about your plant.

- Detailed Plant Layout – This will provide architectural drawings of the plant, including storage areas, Dismantling and segregation linesDismantling And Segregation LinesIndustrial facilities that disassemble and sort waste into separate material streams for recovery and processing., hazardous waste storage and management rooms, and other areas.

- Process Flow Chart and Material Balance – This is a schematic tracking of the process flow your plant will use, with details on inputs, outputs, and losses at each stage.

- Pollution Control Design Specifications – This includes engineering blueprints of proposed Air Pollution Control DevicesAir Pollution Control DevicesEquipment that captures and removes pollutants from industrial exhaust to meet air quality regulations. like bag filters, cyclone separators, etc., and ETP specificationsETP SpecificationsTechnical standards governing the design, construction, and performance of industrial wastewater treatment plants.

- CTE Compliance Report – A written verification and a copy of the CTE that was granted.

- Proof of machinery setup – commercial invoices, structural layout drawings, and physical photographs/videos of the installed recycling machinery

- Environmental Analysis Reports: You will need to verify that your plant operates within the National Ambient Air Quality Standards (NAAQS)National Ambient Air Quality Standards (NAAQS)Regulatory limits on outdoor air pollutant concentrations enforced by India’s CPCB. and effluent discharge limits. For this, you will need to get laboratory test certificates from an MoEF&CC-recognized or NABL-accredited laboratoryNABL-Accredited LaboratoryNABL accreditation confirms a laboratory’s technical competence and compliance with international quality standards for reliable test results. [25].

- Hazardous Waste Authorisation (FORM 1): This document details how hazardous waste generated at your plant will be managed.

- TSDF Agreement: This is your agreement with the business entity that will manage your non-recyclable e-waste components.

- Factory License and Fire Safety Clearances

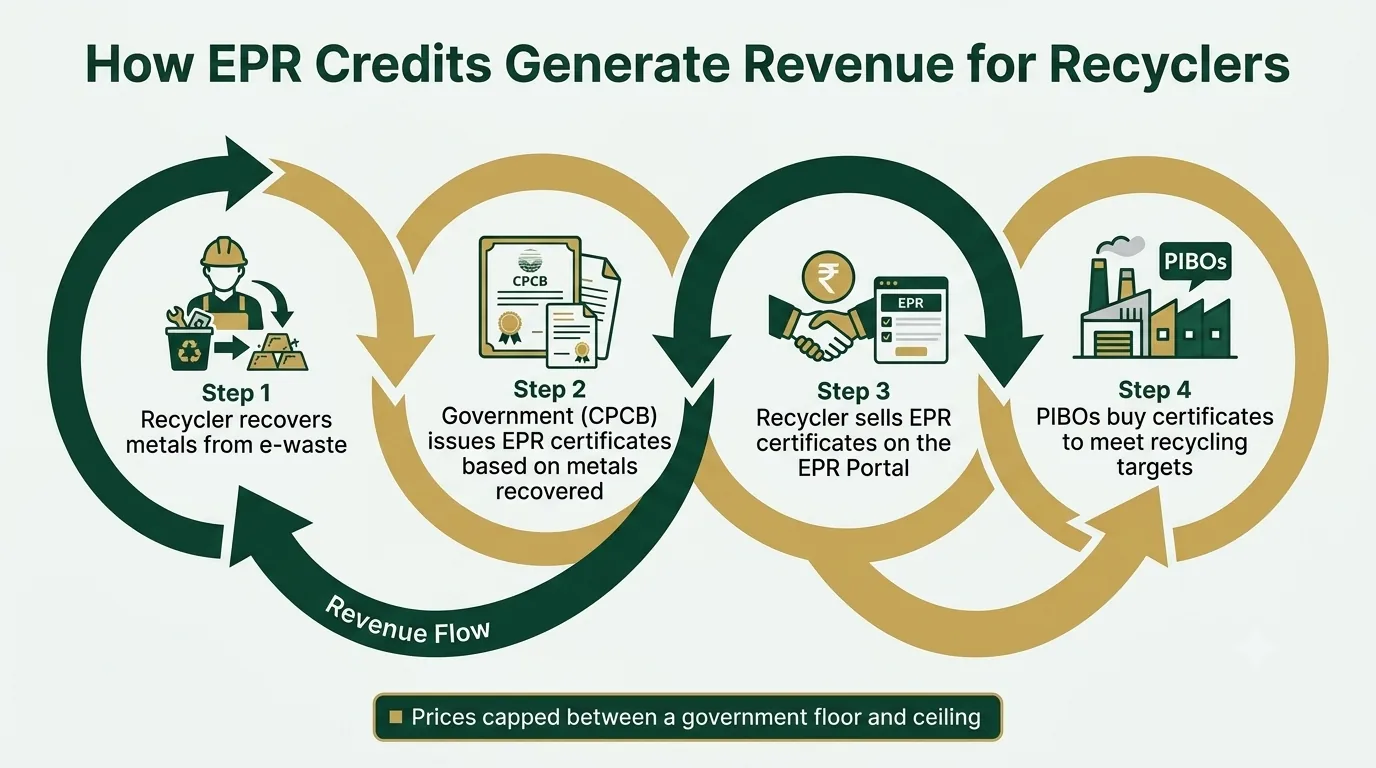

6.3 Extended Producer Responsibility:

Let us first understand what EPR is. As the term suggests, it is an extended producer responsibility. The word producer is the key here. This shifts the responsibility for safe disposal to Producers, Importers, and Brand Owners for any electronic or electrical item introduced into India. These three entities, together, are commonly referred to as PIBOs (Producers, Importers, and Brand Owners). For each piece of equipment, these entities are given a recycling target they must meet. To meet these targets, they purchase something called EPR certificates from e-waste recyclers. As a recycler, you get EPR certificates from the government for the amount of metals you recover by recycling e-waste. Based on the amount of metals recovered, you will get EPR certificates, which you can sell to the PIBOs.[26] Under Rule 4 of the E-Waste (Management) Rules, 2022, a recycler must register on the centralised EPR portal. All your EPR certification generation, trading, tracking, and other activities will take place on this portal. EPR is crucial for a recycler because it provides you with an additional source of revenue for your business. However, EPR certificate prices have a floor and a ceiling, so you can only sell them within a price range set by the government [27].

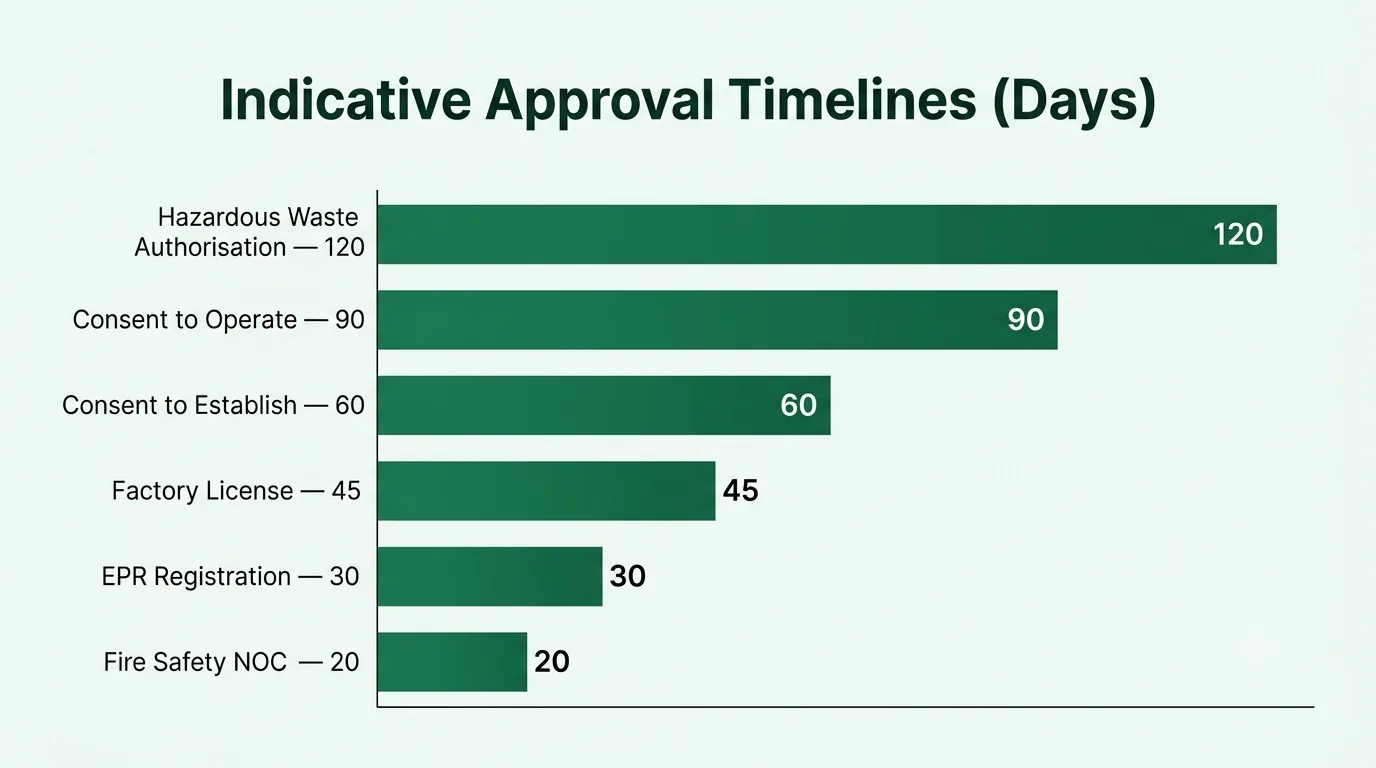

6.4 Approval Bodies and Indicative Timelines

| Approval Body | License / Certificate | Indicative Timeline* | Legal Framework Baseline |

|---|---|---|---|

| SPCB / PCC | Consent to Establish (CTE) | ~60 Days | Air Act 1981 / Water Act 1974 |

| SPCB / PCC | Consent to Operate (CTO) | ~90 Days | Air Act 1981 / Water Act 1974 |

| SPCB / PCC | Hazardous Waste Authorization | ~120 Days | HOWM Rules 2016 |

| Directorate of Factories | Factory License | 30 to 60 Days | Factories Act 1948 |

| State Fire Services | Final Fire Safety NOC | 15 to 30 Days | NBC 2016 / State Fire Acts |

| CPCB (Central) | EPR Portal Recycler Registration | 30 Working Days | E-Waste (Management) Rules, 2022 |

Indicative processing times, not statutory guarantees. Actual timelines vary by state, the authority’s workload, and the completeness of the application. Confirm with the specific authority.*

7. E-waste Recycling Plant Location and Infrastructure Setup

Choosing the right location and infrastructure setup is critical. If you do not have enough nearby feedstock, your transport costs will be higher. Key factors to consider are below.

7.1 Critical Site Selection Factors

- Land type and zone: The land should be industrial. Use the Orange Zone for a mechanical setup, or the Red Zone for pyrometallurgical or hydrometallurgical setups. Starting with a mechanical setup in the Red Zone allows future expansion, but the Red Zone has stricter regulations [28].

- Area of land: When deciding how much land to buy, include space for a greenbeltGreenbeltVegetation buffer used to mitigate air pollution around industrial facilities and urban areas. and future expansion.

- Feedstock estimate: Survey the area and understand the neighbourhood. Check nearby industries, population density, residential-to-industrial ratio, and recycler density to estimate the types and amounts of feedstock available.

- Proximity to end-product consumers: Your end products are ferrous, non-ferrous, and precious metalsPrecious MetalsGold, silver, and platinum-group metals (Pd, Pt, Rh). The primary economic driver in PCB recycling — concentrations in mobile phone PCBs can exceed natural gold ore by 40-50x.. Locating near industries that use these as raw materials reduces transport costs and can improve your margins.

- Infrastructure availability: Power, water, and road connectivity are essential. Reliable power and water keep your plant running, and good road access supports logistics.

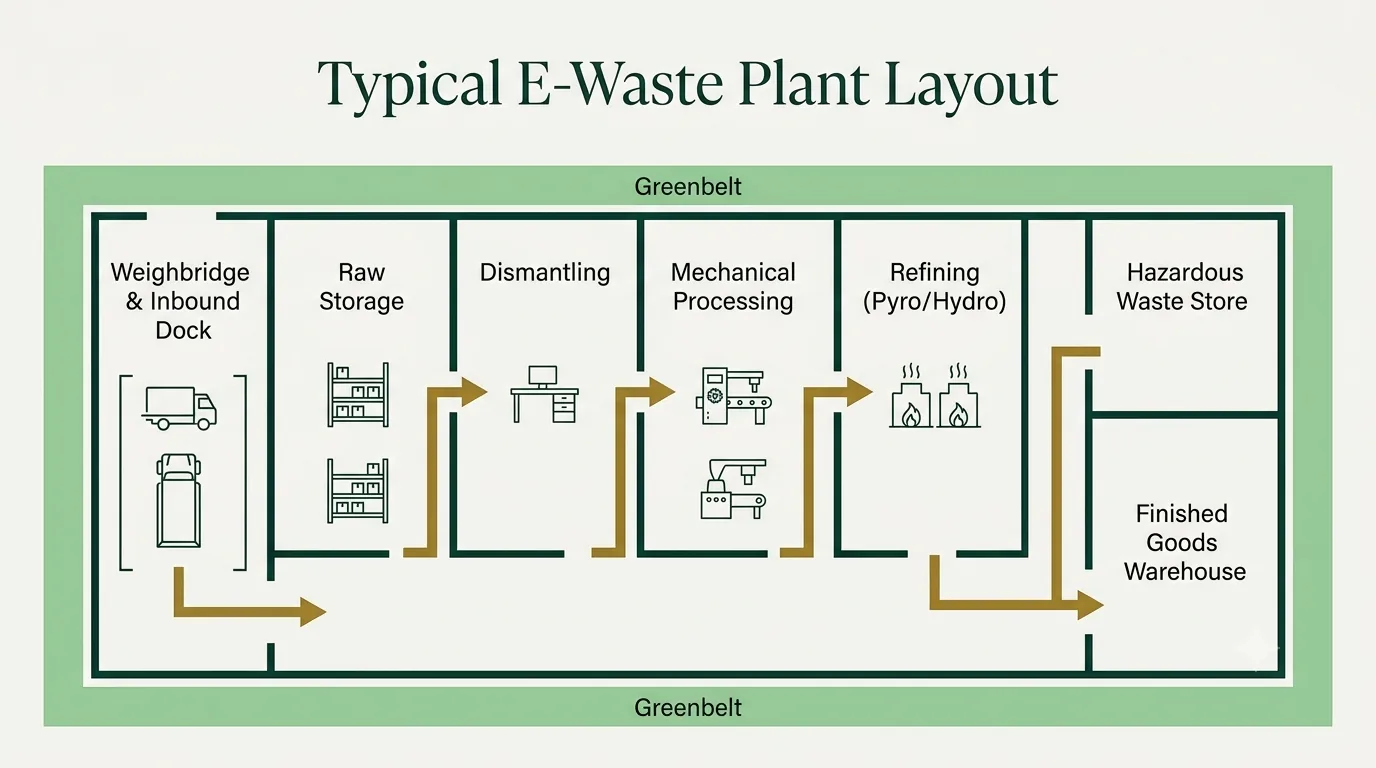

7.2 Internal Facility Zoning and Infrastructure Mapping

It is also important to know the different zones in your plant. The zones in your plant will largely depend on the nature of the e-waste recycling plant you set up. Below you can find a table that details different zones in a plant depending on the plant variant –

| Factory Zone / Area | Tier 1 | Tier 2 | Tier 3 | Tier 4 |

|---|---|---|---|---|

| Weighbridge & Inbound Loading Dock | ✓ | ✓ | ✓ | ✓ |

| Raw E-Waste Storage Area (Unsorted) | ✓ | ✓ | ✓ | ✓ |

| Manual Dismantling Benches | ✓ | ✓ | ✓ | ✓ |

| Localized Dust & Fume Extraction System | ✓ | ✓ | ✓ | ✓ |

| Acoustic (Soundproof) Enclosure Zone | X | ✓ | ✓ | ✓ |

| Impermeable Acid-Resistant Epoxy Flooring | ✓ | ✓ | ✓ | ✓ |

| Chemical Leaching & Acid Treatment Tanks | X | X | X | ✓ |

| Pulse-Jet Bag Filters & Cyclone Dust Collectors | X | ✓ | ✓ | ✓ |

| Wet Scrubbers with Alkaline Dosing Columns | X | ✓ | ✓ | ✓ |

| Effluent Treatment Plant (ETP) | X | X | X | ✓ |

| Secure Hazardous Waste Storage Room | ✓ | ✓ | ✓ | ✓ |

| Finished Commodities Warehouse | ✓ | ✓ | ✓ | ✓ |

Tier 1: Collection & Dismantling Tier 2: Pure Mechanical (Ferrous Mix) Tier 3: Advanced Mechanical (Multi-Metal) Tier 4: Fully Integrated (Mech + Pyro + Hydro) This is an indicative infrastructure map by plant type, not a statutory classification, and exact requirements follow from your process design and SPCBSPCBState Pollution Control Board — the state-level statutory authority that issues, monitors, and enforces environmental consents for industrial plants. conditions. When you choose a plant location, consider plant type, feedstock, zone, and the surrounding area together. If one factor is wrong, the whole setup can fail.

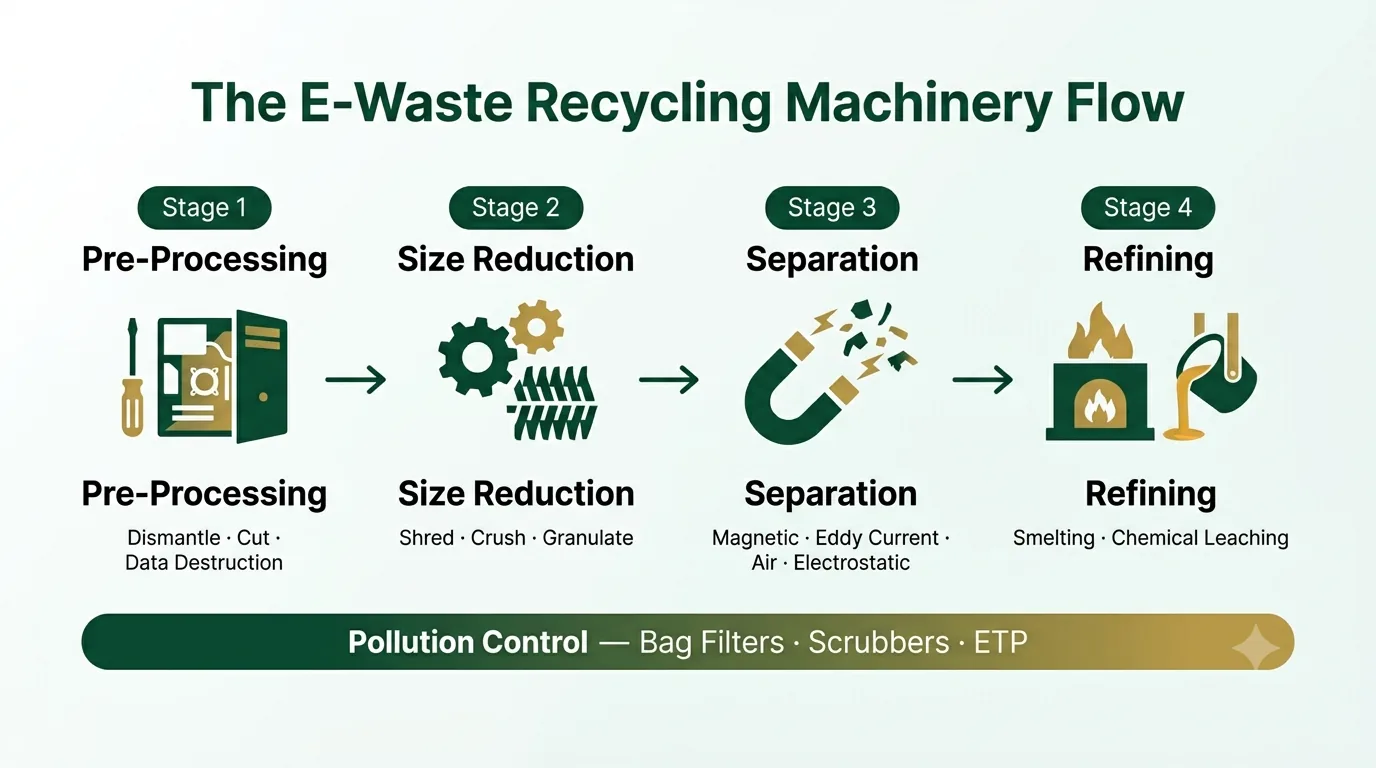

8. Essential E-waste Recycling Machinery and Equipment List

Machinery and equipment are central to an e-waste recycling business. You can group them by their role in the process.

8.1 Upstream & Pre-Processing:

You need these machines for all plant variants. They dismantle, sort, and segregate electronic scrap. They also handle data destruction for hardware like HDDs and magnetic drives.

- Dismantling Workstations – Used for preliminary separation of scrap.

- Component Removing Machine (CRM)Component Removing Machine (CRM)Automated equipment used to separate materials from waste products before recycling. / Depopulator – Helps detach chips, capacitors, and processors from PCBs without damage.

- Pneumatic Toolkits & Industrial De-soldering StationsIndustrial De-soldering StationsEquipment used to non-destructively remove components from circuit boards for reuse or further material recovery. – These are used for mechanical stripping of frames from the rest of the body.

- Specialised Cutters – These help with cutting activities such as stripping cables and wires, cutting CRT/LCD screens, etc.

- Data Destruction UnitsData Destruction UnitsEquipment that securely destroys data on storage devices before recycling electronics. – These are used to clean data from hardware devices that could contain sensitive information. There are Hard Disk Drive (HDD) Degaussing, Solid-State Drive (SSD) Physical ShreddingSolid-State Drive (SSD) Physical ShreddingIndustrial shredding of SSDs for secure data destruction and material recovery in e-waste recycling., etc.

8.2 Mechanical Size Reduction Machinery:

These machines reduce the size of the feedstock, allowing you to separate components.

- Shredders: Shred electronic scrap into smaller flakes. Depending on the setup requirement, you can choose between a single-shaft shredderSingle-Shaft ShredderIndustrial machine with a single rotating shaft used to shred and size-reduce various waste materials., a double-shaft shredderDouble-Shaft ShredderIndustrial machine using two counter-rotating shafts with blades to shred and size-reduce waste materials. or a quad-shaft shredderQuad-Shaft ShredderFour-shaft industrial machine that shreds and size-reduces waste materials for recycling applications..

- CrushersCrushersMechanical equipment used to break down waste materials into smaller pieces for recycling operations.: After Shredders break scrap down into smaller bits, crushers like a hammer mill further break it down into smaller sizes.

- GranulatorsGranulatorsMachines that cut waste materials into uniform granules for downstream recycling processes./Grinders: These are used to grind materials into tiny fractions. These are particularly important when working with PCBs, where the mechanical bond between copper foils and fibre glass is broken.

8.3 Advanced Material Separation Systems:

- You use these to separate material into categories like ferrous, non-ferrous, precious metals, and plastic.

- Magnetic SeparatorsMagnetic SeparatorsEquipment that uses magnetic fields to remove ferrous metal contaminants from feedstock materials.: These are used to separate ferrous metals from a mixture using a strong magnet that pulls them out of the stream.

- Eddy Current Separators (ECS)Eddy Current Separators (ECS)Equipment using electromagnetic induction to separate non-ferrous metals from non-metallic waste materials.: These are based on the principle of using a magnetic field to induce eddy current and separate non-ferrous metalsNon-Ferrous MetalsMetals containing no iron — copper, aluminium, zinc, lead, tin, nickel and precious metals. Non-magnetic and the highest-value recoverable fraction of e-waste. from the mixture.

- Air Density SeparatorAir Density SeparatorPhysical separation equipment that uses airflow to segregate materials by density.: Works on the principle of separating based on different densities of the mixture. These are used to separate plastics from heavier metal fractions.

- Electrostatic separatorElectrostatic SeparatorDevice using electric fields to separate charged particles from mixed granular waste streams.: Used in PCB processing to separate metallic copper dust from non-metallic resin powder.

8.4 Downstream Metal Extraction and Refining Technologies:

You use this setup to obtain pure metals. Pyrometallurgy uses heat or smelting to recover metals as ingots. Hydrometallurgy uses chemical leachingLeachingA hydrometallurgical process that dissolves target metals out of crushed e-waste into an aqueous chemical solution using acids, cyanide or other reagents, for later recovery..

- Chemical Leaching ReactorsChemical Leaching ReactorsIndustrial vessels that dissolve target materials from solids using chemical solvents under controlled conditions.: These are temperature-controlled agitation tanks that are used in hydrometallurgy. These selectively dissolve and separate precious metals such as gold, silver, and Palladium.

- Smelting/Induction FurnacesInduction FurnacesElectric furnace using electromagnetic induction to melt metals and conductive materials.: These furnaces are used to melt metals with flux and heat them to high temperatures to produce metal ingots. This process is referred to as pyrometallurgy.

8.5 Pollution Control Equipment and Emission Standards:

The recycling process generates air pollution and harmful effluents. You need effective pollution management to comply with regulations. Key equipment includes pulse-jet bag filters, cyclone dust collectorsCyclone Dust CollectorsEquipment that separates dust particles from gas streams using spinning motion to protect air quality and equipment., wet scrubbers with alkaline dosing columnsAlkaline Dosing ColumnsEquipment for controlled addition of alkaline agents to adjust pH and facilitate chemical reactions in waste-to-value processes., effluent treatment plants (ETP), and acoustic enclosures. Mechanical processing also releases gas-phase toxins a dry filter can’t trap — mercury and phosphor from CRT/LCD cutting, and lead-tin and brominated flame-retardant fumes from desoldering. CPCB’s SOPs for e-waste recyclers require gas-phase emission control on these streams, which is why wet scrubbersWet ScrubbersAir pollution control devices that use liquid to capture particulate matter and gaseous pollutants from exhaust streams. are needed from Tier 2, not just at the chemical stage [29].

8.6 Centralised Machinery Deployment Matrix:

The table below shows which machinery setups are needed for different plant types. This is only indicative; your exact machinery will depend on your final process flow.

| Machinery / Equipment Name | Tier 1 | Tier 2 | Tier 3 | Tier 4: |

|---|---|---|---|---|

| Upstream & Pre-Processing | ||||

| Dismantling Workstations with Suction | ✓ | ✓ | ✓ | ✓ |

| Component Removing Machine (CRM) / Depopulator | X | ✓ | ✓ | ✓ |

| Specialised Cutters | ✓ | ✓ | ✓ | ✓ |

| Data Destruction Units | ✓ | ✓ | ✓ | ✓ |

| Size Reduction & Granulation | ||||

| Shredder | X | ✓ | ✓ | ✓ |

| Crusher | X | ✓ | ✓ | ✓ |

| Granulator / Grinder | X | X | ✓ | ✓ |

| Advanced Material Separation | ||||

| Magnetic Separator | X | ✓ | ✓ | ✓ |

| Eddy Current Separator | X | X | ✓ | ✓ |

| Air Classifier / Air Density Separator | X | X | ✓ | ✓ |

| High-Voltage Electrostatic Separator | X | X | ✓ | ✓ |

| Downstream Refining & Metal Extraction | ||||

| Chemical Leaching Reactors | X | X | X | ✓ |

| Smelting / Induction Furnaces | X | X | X | ✓ |

| Pollution Control & Auxiliary Safety | ||||

| Pulse-Jet Bag Filters & Cyclone Dust Collectors | X | ✓ | ✓ | ✓ |

| Wet Scrubbers with Alkaline Dosing Columns | X | ✓ | ✓ | ✓ |

| Closed-Loop Effluent Treatment Plant (ETP) | X | X | X | ✓ |

| Acoustic (Soundproof) Machine Enclosures | X | ✓ | ✓ | ✓ |

| Impermeable Acid-Resistant Epoxy Flooring | ✓ | ✓ | ✓ | ✓ |

Tier 1: Collection & Manual Dismantling Tier 2: Pure Mechanical (Ferrous Mix) Tier 3: Advanced Mechanical (Multi-Metal) Tier 4: Fully Integrated (Mech + Pyro + Hydro)

8.7 Throughput Capacity and Engineering Synergy Conclusion

Choose your equipment based on your plant’s process flow. Finalise the plant variant and process flow first, then select machinery. If you want higher purity metals, you will need more processing and pollution control. Machinery specs like throughput, working hours, and rest time depend on plant capacityPlant CapacityThe maximum volume of material a facility can process or produce per unit time, measured in tons per day or tons per year..

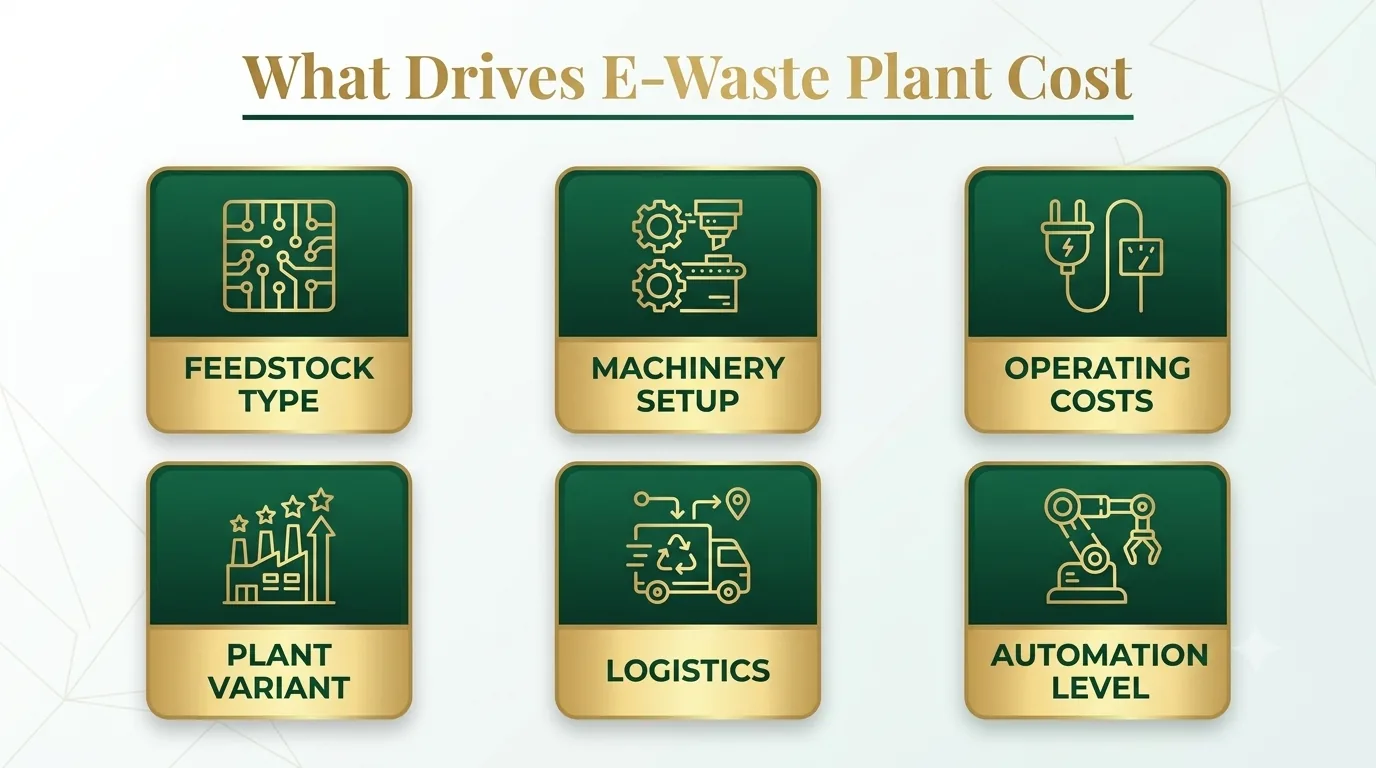

9. What Determines the Cost of an E-Waste Recycling Plant

The cost of an e-waste recycling setup depends on the plant variant. A simple collection and dismantling setup costs ₹60–80 lakh. A plant with full mechanical, hydrometallurgical, and pyrometallurgical processes costs ₹2–3 crore.

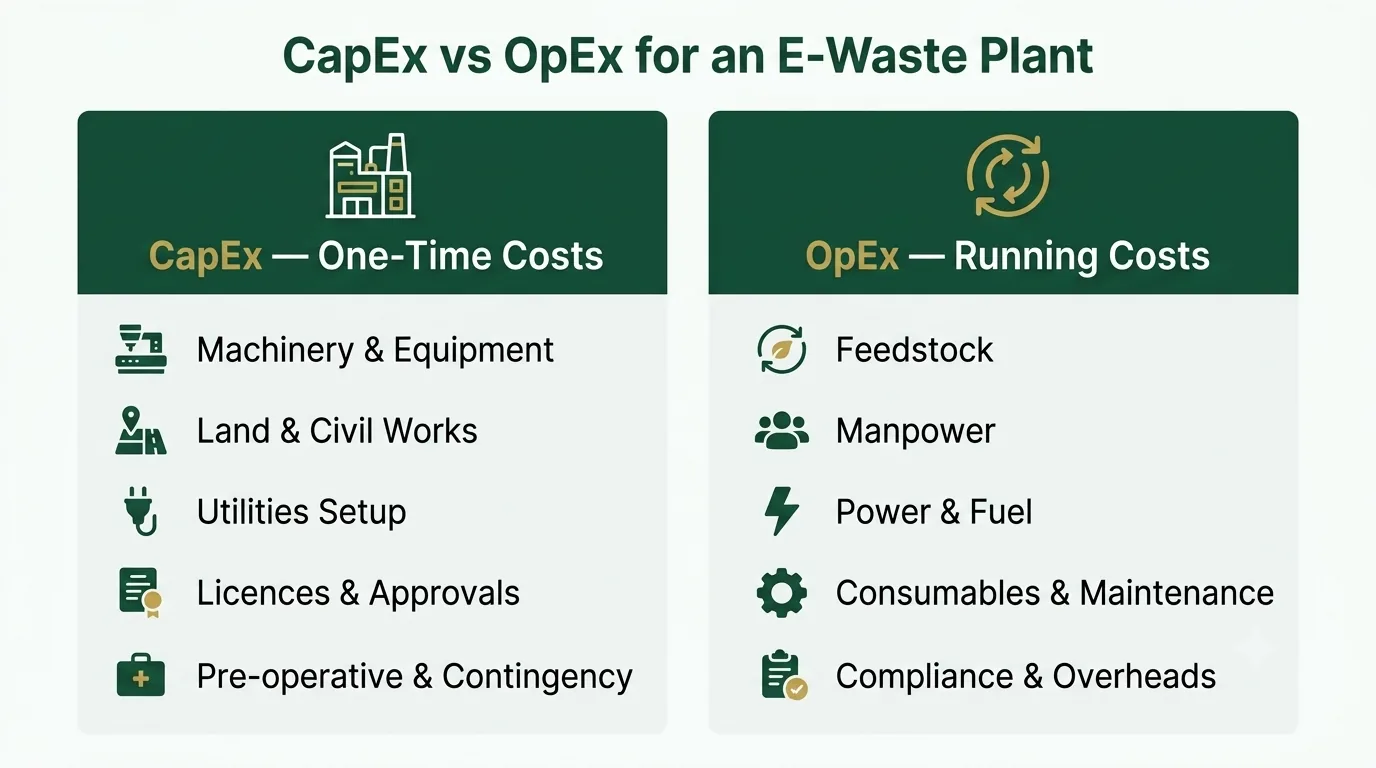

The main factors that decide the economics of an e-waste recycling plant are capital expenditure (capex), operating expenditure (opex), return on investment (ROI), and profit. Feedstock: Feedstock is the raw material processed in an e-waste recycling plant. The CPCBCPCBCentral Pollution Control Board — India’s apex statutory body for environmental regulation, constituted under the Water Act, 1974. identifies over 120 types of e-waste. The type of feedstock you select depends on its metal concentration and the plant design. Feedstock with high precious metal content, such as PCBs and motherboards, costs more than common electronic scrap, such as washing machines and fridges [30]. The source of feedstock also affects cost. Scrap from dealers and dismantlers costs more than sourcing directly from producers and manufacturers. Machinery Setup: Machinery types fall into three categories: mechanical, hydrometallurgical, and pyrometallurgical. Mechanical machinery is cheaper. Pyrometallurgical and hydrometallurgical setups cost much more. Hydrometallurgical and pyrometallurgical setups also need larger auxiliary systems, such as Effluent Treatment Plants (ETPs) and air purification systems [31]. Operating Costs: Operating costs, including electricity and water, depend on the number of hours the plant runs. Choosing machinery with lower power and water use reduces these costs. Plant Variant: E-waste recycling plants can take different forms. Collection and dismantling plants are the cheapest to set up. Mechanical plants produce mixed fractions of precious metals, ferrous metals (iron and steel alloys), and non-ferrous metals (copper and aluminium alloys). (E-waste Recycling Plant – Refnic, 2023) These cost more than collection and dismantling plants. To obtain pure ferrous and non-ferrous metals, a pyrometallurgical setup is required. For pure precious metals, a hydrometallurgical setup is needed. Both are extensions of the mechanical setup. (Harvey et al., 2016) As you move from mixed fractions to pure metals, your investment goes up, but the end product is worth more. Set up Infrastructure: Plant setup infrastructure depends on the plant variant and the quality of materials you use. Logistical Cost: Transport is a key factor in e-waste recycling. Waste is often sourced from different states and moved over long distances. Transport costs have a major impact on plant economics. Higher automation reduces operating costs and worker requirements but increases machinery setup costs.

10. Comprehensive Capital Expenditure (CapEx) Metrics

The table below provides a basic breakdown of CapEx costs.

| CapEx Component | Tier 1: Collection & Dismantling (₹ Lakhs) |

|---|---|

| Machinery & Core Equipment | ₹12.00 |

| Land, Site Layout & Civil Works | ₹15.00 |

| Pollution Control & Air/Liquid Safety | ₹3.00 |

| Utilities, Power Setup & Diesel Generators | ₹5.00 |

| Pre-operative Expenses & Contingency | ₹3.00 |

| Statutory Approvals & SPCB/CPCB Licences | ₹2.00 |

| Total Estimated Project CapEx | ₹40.00 Lakhs |

| Output Commodity Type | Sorted components & raw plastic casing |

| CapEx Component | Tier 2: Pure Mechanical (Ferrous Mix) (₹ Lakhs) |

|---|---|

| Machinery & Core Equipment | ₹35.00 |

| Land, Site Layout & Civil Works | ₹25.00 |

| Pollution Control & Air/Liquid Safety | ₹12.00 |

| Utilities, Power Setup & Diesel Generators | ₹10.00 |

| Pre-operative Expenses & Contingency | ₹5.00 |

| Statutory Approvals & SPCB/CPCB Licences | ₹3.00 |

| Total Estimated Project CapEx | ₹90.00 Lakhs |

| Output Commodity Type | Mixed Ferrous scrap & loose PCB fractions |

| CapEx Component | Tier 3: Advanced Mechanical (Multi-Metal) (₹ Lakhs) |

|---|---|

| Machinery & Core Equipment | ₹65.00 |

| Land, Site Layout & Civil Works | ₹35.00 |

| Pollution Control & Air/Liquid Safety | ₹18.00 |

| Utilities, Power Setup & Diesel Generators | ₹12.00 |

| Pre-operative Expenses & Contingency | ₹7.00 |

| Statutory Approvals & SPCB/CPCB Licences | ₹5.00 |

| Total Estimated Project CapEx | ₹142.00 Lakhs |

| Output Commodity Type | Cleaned Ferrous, Non-Ferrous (Cu/Al), & PCB concentrate |

| CapEx Component | Tier 4: Fully Integrated (Mech + Pyro + Hydro) (₹ Lakhs) |

|---|---|

| Machinery & Core Equipment | ₹175.00 |

| Land, Site Layout & Civil Works | ₹65.00 |

| Pollution Control & Air/Liquid Safety | ₹45.00 |

| Utilities, Power Setup & Diesel Generators | ₹25.00 |

| Pre-operative Expenses & Contingency | ₹15.00 |

| Statutory Approvals & SPCB/CPCB Licences | ₹10.00 |

| Total Estimated Project CapEx | ₹335.00 Lakhs |

| Output Commodity Type | Bullion Gold/Silver and bulk Copper/Aluminium/Steel ingots |

| CapEx Component | Collection & Dismantling | Mechanical | Mechanical + Hydro/Pyro |

|---|---|---|---|

| Machinery & equipment | 25–35% | 45–55% | 50–60% |

| Land & civil works | 25–35% | 20–30% | 15–25% |

| Pollution control & safety | 5–10% | 8–15% | 15–25% |

| Utilities & electrical infra | 8–12% | 8–12% | 8–12% |

| Pre-operative & contingency | 8–12% | 5–10% | 5–8% |

| Licences & approvals | 5–8% | 3–6% | 2–5% |

| Plant Variant | Total Capex |

|---|---|

| Collection & Dismantling | ₹40.00 Lakhs |

| Pure Mechanical (Ferrous Mix) | ₹90.00 Lakhs |

| Advanced Mechanical (Multi-Metal) | ₹142.00 Lakhs |

| Fully Integrated (Mech + Pyro + Hydro) | ₹335.00 Lakhs |

11. Operational Expenditure (OpEx) Factors

The table below provides a basic breakdown of OpEx costs.

| OpEx Factor | Collection & Dismantling | Mechanical | Mechanical + Hydro/Pyro |

|---|---|---|---|

| Power / electricity | Low | High | Very High |

| Water | Low | Low–Medium | High |

| Chemicals / consumables | Very Low | Low | Very High |

| Maintenance & spares | Low | Medium | High |

| Pollution control & effluent treatment | Low | Medium | Very High |

| Compliance & monitoring | Low | Medium | High |

| Safety & PPE / hazard handling | Low | Medium | High |

Disclaimer: The CapEx and OpEx financial metrics above use standard 2026 industrial manufacturing averages in India and are only a preliminary feasibility guide. Actual plant setup costs will vary based on local land rates, machinery suppliers, import duties on technology, and state-level subsidies. Consult a certified project engineer and Chartered Accountant for a tailored Project Report (DPR) before you invest.

12. E-waste Recycling Plant Setup: Step-by-Step Execution Guide

Follow the steps in order to set up an e-waste recycling plant. Step 1: Understand the business. You need a basic understanding of the domain before you begin. Free resources are available online. For in-depth and structured information, Adhara-Viveka provides resources on the e-waste recycling business. Step 2: Market survey. Contact vendors for machinery, regulatory services, plant setup, and feedstock. This step provides you with ground data and a practical understanding. Many skip steps 1 and 2, but they are crucial. Price and service volatility are high in e-waste, so get the numbers yourself. Step 3: Consultancy and reports. You can outsource the project to an EPC contractorEPC ContractorA contractor responsible for complete design, procurement, and construction of waste-processing plants. or hire a consultant and stay involved. If you outsource, later steps may not apply, but you should still understand them. If you work with a consultant, use your knowledge from steps 1 and 2 to finalise plant capacity and variant. Step 4: Feasibility report. After step 3, prepare a feasibility report or business plan. Use your own data and knowledge from earlier steps, not just the consultant’s input. The report should help you decide whether to proceed, using real numbers. Step 5: Business registration. If the numbers from step 4 are viable, register your business. Step 6: Location analysis. Finalise the plant location and procure land. If you have done the market survey properly, this step should be straightforward. Step 7: Detailed Project Report and CTE. After finalising specifics and procuring land, prepare a Detailed Project Report (DPR). Once ready, apply for Consent to EstablishConsent to EstablishConsent to Establish — a regulatory approval issued by the State Pollution Control Board allowing an industrial plant to be set up at a specific location. (CTE). Hydrometallurgical or pyrometallurgical setups also need EIA clearanceEIA ClearanceRegulatory approval required in India for projects assessed to have significant environmental impact.. (E-Waste (Management) Rules, 2022, 2022) Step 8: Civil works, machinery procurement, and pre-commissioning regulatory work. After you get CTE, start plant construction and procure machinery. Once complete, apply for pre-commissioning licences and certificates. Step 9: EPR Portal Registration, Feedstock Procurement, and Trial Run – Register as a recycler on the EPR portal, procure feedstock for at least three months, and conduct a trial run.

13. E-waste Recycling Business Plan

A business plan outlines your planned execution and expected economic results. Prepare a detailed business plan before starting an e-waste recycling business.

A business plan provides clarity on the following aspects:

13.1 Project Cost / Capital Required –

- Working capital: Working capital covers costs you incur before the plant generates revenue. You pay for scrap upfront, but revenue comes only after you sell EPR certificates and recovered materials. Working capital protects you against these revenue gaps. Electronic scrap prices are volatile, and precious metals like gold and silver can drop suddenly. Working capital is your buffer.

- Machinery & equipment cost: This is the cost for your machinery and equipment setup. Include not just the machinery, but also installation, setup, and transport. As you move from manual processing to advanced processes like pyrometallurgy and hydrometallurgy, costs increase. Higher automation also raises costs.

- Land, site layout & civil works: Civil works include costs for boundary walls, internal roads, office blocks, and more. Land costs depend on whether you buy or lease. Site layout covers flooring type, storage areas, and other features.

- Utilities Cost: This includes your utility costs, such as power setup, diesel generators, and wiring and cabling.

- Pre-operative Expenses & Contingency: Pre-operative costs are incurred before commercial production, such as a trial run, staff salaries during setup, and consultant fees. Contingency is a buffer amount in case of any unanticipated expenses.

- Statutory Approvals & SPCB/CPCB Licences: This would include costs incurred for licences and certifications, such as CTE, CTO, and EPR registrationEPR RegistrationMandatory registration process for producers and importers to manage post-consumer waste and meet Extended Producer Responsibility obligations..

- Other Capex Costs: These are not major capex costs; they should still be well accounted for: material handling equipment, weighbridge, IT, Software & Surveillance, Lab & Testing Equipment, Fire-fighting system.

13.2 Operating Costs (Opex)

- Feedstock/Raw Material Cost: This is the price you pay to purchase electronic scrap to be processed in your plant. It is important to note that there is no standard central monitoring body for scrap prices, and the sector is largely dominated by the informal sector. Additionally, it is important to include the landing cost in the calculation, not the pickup price.

- Manpower: This will be labour and salary expenses. Higher automation will reduce manpower costs and increase efficiency. The level of automation in your dismantling lineDismantling LineA series of workstations where electronic waste is systematically taken apart to recover materials and isolate hazards. can make the difference between a large manual labour team and a lean one.

- Power and Fuel: These will be electricity charges, diesel for DG sets, fuel for forklifts and vehicles, etc.

- Consumables, Maintenance & Logistics: This includes PPE, spares, packaging, tools, routine repairs, etc

- Compliance & Pollution-Control Running Costs: These include costs such as CTO renewal, EPR reporting, ETP chemicals, and related expenses. The non-recyclable components will be going to TSDF, and those costs also need to be accounted for.

- Overheads & Finance: These are different Overheads and financial costs, like Office/admin expenses, IT and EPR software subscriptions, insurance, etc

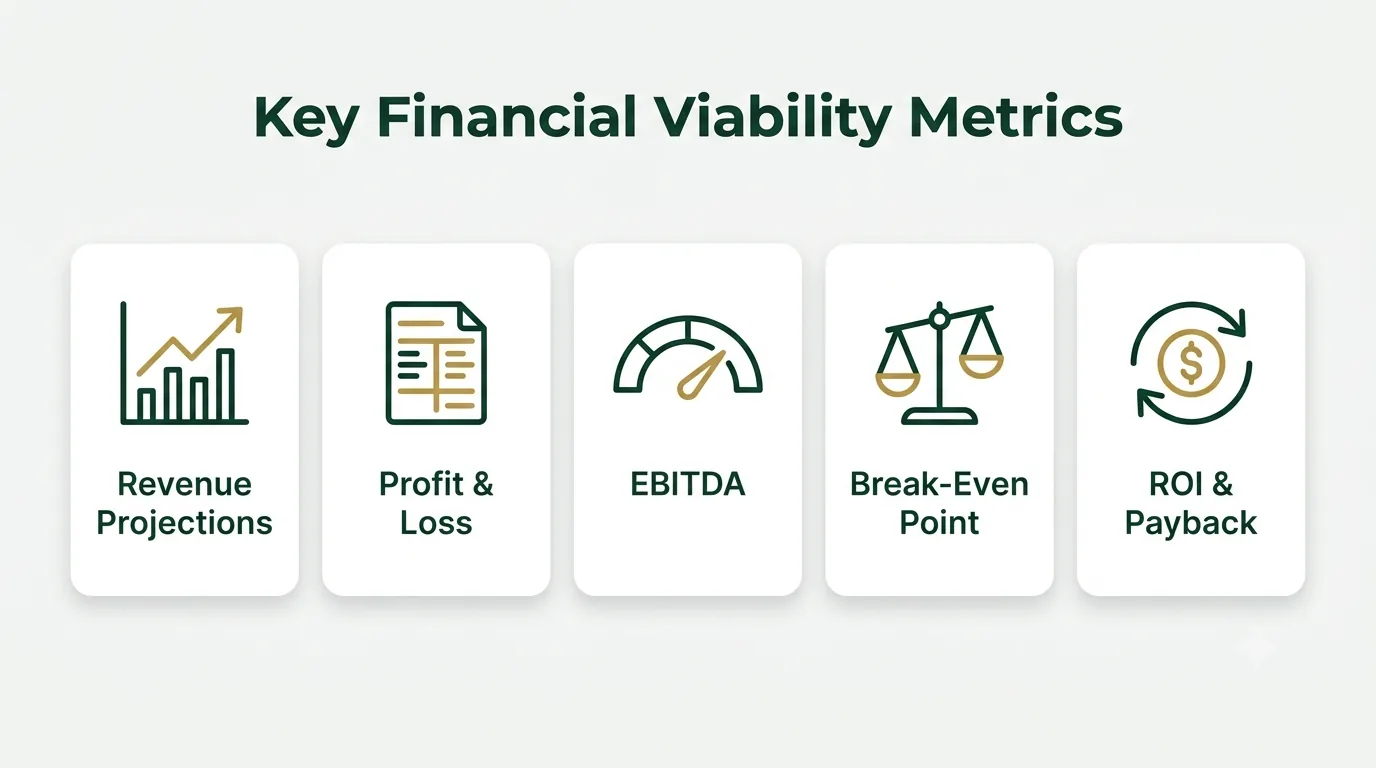

13.3 Financial Projections & Viability:

Financial projections tell you how your business will perform. This includes profit and loss statements, forecasted revenue, and related information. Viability indicates whether your business logic is sound.

- Revenue Projections: This covers the revenue you can expect from the sale of recovered materials and EPR certificates. While revenue is largely dictated by international metal exchanges such as the LME and LBMA, EPR is a policy-driven setup, and the prices of EPR certificates have a ceiling and a floor. Revenue from any other source belongs here, too.

- Profit & Loss (P&L) Statement: This shows how much money you will be left with after subtracting your OPEX from your Revenue. Profits can take many forms, including gross profit, operating profit, EBITDA, profit before tax, and net profit.

- EBITDA: EBITDA is Earnings Before Interest, Tax, Depreciation and Amortisation. It provides a clean measure of operating profitability, excluding financing and accounting effects, and helps assess your plant’s operating health.

- Breakeven Analysis: Break-even is the point at which you stop making a loss. This is particularly important because it tells you at which stage your plant will be self-sufficient.

- ROI / Payback Period: The payback period tells you how long it will take to recover the capital you invested in the plant. ROI, on the other hand, is a measure of how much profit you make relative to the money you put in. It tells you how much you get back for every rupee you invest.

A business plan is not just about numbers. It is about what those numbers show. Some costs, like machinery, civil works, and licence fees, are fixed. Key variables like feedstock prices and recovery yields are uncertain and often change. Your plan should account for this uncertainty. Use conservative estimates for these variables.

14. Challenges and Risk Mitigation for E-waste Recycling Plant in India:

When you start an e-waste recycling business, you need to know the main challenges and how to manage them. A sound plan covers both the opportunity and the risks. Here are some key areas where you need to understand the risks and how to reduce them.

14.1 Supply-Chain & Procurement Risk:

Despite India generating a large amount of e-waste, much of which is not recycled, many recyclers struggle to find feedstock. Informal parallel sectors, such as unregistered scrap dealers/kabadiwalas in hubs like Seelampur, Dharavi, or Moradabad, command the vast majority of the collection network. Mitigation: As a recycler, you must build a multi-tier, robust network for feedstock collection. The more diverse and wide-ranging collection structures you build, the better your feedstock procurement will be. Set up collection hubs in your operating area and secure long-term contracts directly with PIBOs (Producers, Importers and Brand Owners).

14.2 Technological Risk: The Material Inhomogeneity & Purity Gap

A major problem in e-waste recycling is the non-uniformity of the feedstock. A wide range of feedstock and multiple recoverable metals increase the complexity of the recovery process [32]. Mitigation: Focus on a limited set of feedstocks instead of pursuing every electronic scrap in the market. Make sure your plant setup is optimised for high-purity recovery and tailored to the feedstock you are working with.

14.3 Occupational Health & Environmental Liability Risks

E-waste contains many hazardous substances that must be handled carefully during dismantling. Additionally, the recycling process also produces toxic gases in the pyro setup and effluents in the hydro setup. This can lead to exposure to harmful contaminants and introduce regulatory problems and community backlash [33]. Mitigation: Implement appropriate safety measures and pollution control systems. Make sure to constantly measure hazardous levels at your plant and properly maintain pollution control devices. Two out of three major challenges are related to feedstock. This shows you need a proper understanding of feedstock and its role. All three challenges are ongoing, not one-time. You need to build systems that keep working to manage these risks.

15. Final Word: Is E-Waste Recycling Worth It?

E-waste recycling is driven by policy, not speculation. Rising EPR targets, government schemes like the National Critical Mineral Mission, and the push to formalise collection points all create mandated demand for compliant capacity. Whether a plant is profitable still depends on feedstock economics and execution. E-waste recycling business success does not depend only on capacity or advanced technology. It depends on how well feedstock, process flow, and target output are aligned. Nearly every decision comes back to two things: the cost and availability of feedstock, and the value you recover from it. This guide helps you understand the key factors. The next step is to plan properly, using a deep understanding and tested numbers. That is where the business is decided.

FAQs: E-Waste Recycling Business in India

Four questions Indian founders ask most about starting an e-waste recycling business. The direct answers below are drawn from the detailed analysis above — treat them as quick reference, and follow the links for the full breakdown.

Is e-waste recycling a profitable business?

Yes, but conditionally. A well-run plant in India operates at 15-30% EBITDA margins with a 2.5- to 4-year payback on capex. Operators who execute three fundamentals well — deliberate input-stream selection biased towards PCB-rich corporate ITAD contracts, recovery yields above 92% on the addressable metal fraction, and a meaningful EPR-backed offtake share — reliably outperform. Operators who treat e-waste recycling as a generic scrap-trading business often struggle in year two when working-capital pressure compounds. See the full e-waste business overview on Adhāra Viveka

What are the 7 Rs of recycling?

The 7 Rs framework — Refuse, Reduce, Reuse, Repair, Repurpose, Recycle and Recover — is the standard hierarchy for waste-management priorities, with each R representing a level of environmental preference. Refuse (do not generate the waste in the first place) is the highest-impact action; Recover (extract energy or residual value from waste that cannot be processed otherwise) is the lowest. An e-waste recycling business operates principally at the Recycle and Recover layers. Talk to an e-waste recycling expert

What is the cost of an e-waste recycling plant in India?

The e-waste recycling plant setup cost in India ranges from roughly ₹60 lakh-1.2 crore for a 1-2 TPD dismantling-and-segregation operation, ₹2-4.3 crore for an integrated 5-10 TPD plant, and ₹7.7-14.5 crore for a 15+ TPD facility with deep mechanical separation. Hydrometallurgical or pyrometallurgical on-site precious-metal recovery adds another ₹4-8 crore on top. The full itemised breakdown by land, machinery, pollution control, licences, working capital and pre-operative costs sits in the dedicated section above.

Can I get money from e-waste?

Yes — both individual sellers and operators can monetise e-waste. As an individual selling end-of-life electronics, expect ₹50-300 for a working laptop, ₹100-1,000 for a working smartphone, and ₹5-25 per kg for general consumer e-waste from authorised collection points or buyback programmes. As an operator running a formal plant, the per-tonne economics are materially better: a tonne of mixed e-waste yields roughly ₹50,000-1,10,000 of recovered material value, and a tonne of PCB-rich corporate e-waste can yield ₹2-3 lakh once concentrated and sold to refiners. Find an e-waste recycling consultant

References

- (2011). Metal Extraction Processes for Electronic Waste and Existing Industrial Routes: A Review and Australian Perspective. MDPI 3(1), pp. 152-170. https://www.mdpi.com/2079-9276/3/1/152 ↩

- Vats, M. C. & Singh, S. K. (2015). Assessment of gold and silver in assorted mobile phone printed circuit boards (PCBs): Original article. Waste Management 45, pp. 280-288. https://doi.org/10.1016/j.wasman.2015.06.002 ↩

- Liu, K., Tan, Q., Yu, J. & Wang, M. (2023). A global perspective on e-waste recycling. Circular Economy 2(1). https://www.sciencedirect.com/science/article/pii/S2773167723000055?via%3Dihub ↩

- (May 6, 2026). India’s E-Waste Management. NEXT IAS. https://www.nextias.com/ca/current-affairs/06-05-2026/e-waste-management-india ↩

- (2026). India E-Waste Management Market Size, Share, Report 2034. IMARC Group. https://www.imarcgroup.com/india-e-waste-management-market ↩

- Dutta, D. & Goel, S. (2021). Understanding the gap between formal and informal e-waste recycling facilities in India. Waste Management 125, pp. 163-171. https://doi.org/10.1016/j.wasman.2021.02.045 ↩

- (2022). E-Waste (Management) Rules, 2022. International Energy Agency. https://www.iea.org/policies/25027-e-waste-management-rules-2022 ↩

- (n.d.). E-Waste (Management) Rules, 2022. https://www.pib.gov.in/Pressreleaseshare.aspx?PRID=1943201&lang=2®=48 ↩

- (2022). E-Waste Management Rules, 2022. International Energy Agency. https://www.iea.org/policies/25027-e-waste-management-rules-2022 ↩

- (September 3, 2025). Cabinet clears ₹1,500 cr scheme to promote critical mineral recycling. Business Standard. https://www.business-standard.com/industry/news/cabinet-approves-rs-1500-crore-scheme-for-critical-mineral-recycling-125090301478_1.html ↩

- Ghimire, H. & Ariya, P. A. (2020). E-Wastes: Bridging the Knowledge Gaps in Global Production Budgets, Composition, Recycling and Sustainability Implications. Sustain. Chem. 2020. https://doi.org/10.3390/suschem1020012 ↩

- (n.d.). Pyrometallurgy. chemeurope.com. https://www.chemeurope.com/en/encyclopedia/Pyrometallurgy.html ↩

- (n.d.). Pyrometallurgy. chemeurope.com. https://www.chemeurope.com/en/encyclopedia/Pyrometallurgy.html ↩

- “Hydrometallurgy.” Chemistry LibreTexts, 2020. https://chem.libretexts.org/Courses/University_of_Missouri/MU%3A__1330H_%28Keller%29/23%3A_Metals_and_Metallurgy/23.3%3A_Hydrometallurgy Accessed July 3, 2026 https://chem.libretexts.org/Courses/University_of_Missouri/MU%3A__1330H_%28Keller%29/23%3A_Metals_and_Metallurgy/23.3%3A_Hydrometallurgy ↩

- Iannicelli-Zubiani, Elena M., Martina I. Giani, Francesca Recanati, Giovanni Dotelli, Stefano Puricelli, and Cinzia Cristiani. “Environmental impacts of a hydrometallurgical processHydrometallurgical ProcessWater-based method for extracting metals from waste materials through leaching and chemical separation. for electronic waste treatment: A life cycle assessment case study.” Journal of Cleaner Production 140 (2017): 1204-1216. Accessed July 3, 2026 https://doi.org/10.1016/j.jclepro.2016.10.040 ↩

- “E-Waste (Management) Rules, 2022.” UNEP Law and Environment Assistance Platform, November 2, 2022. https://leap.unep.org/en/countries/in/national-legislation/e-waste-management-rules-2022 ↩

- “E-Waste (Management) Rules, 2022.” UNEP Law and Environment Assistance Platform. 2022. Accessed July 3, 2026 https://leap.unep.org/en/countries/in/national-legislation/e-waste-management-rules-2022 ↩

- Chakraborty, S., Qamruzzaman, M., Zaman, M., Alam, M. M., Hossain, M. D., Pramanik, B., Nguyen, L., Nghiem, L., Ahmed, M., Zhou, J., Mondal, M. I., Hossain, M., Johir, M., Ahmed, M., Sithi, J., Zargar, M. & PhD, M. A. (2022). A review on recovery processes of metals from E-waste: A green perspective. Science of the Total Environment 850. https://www.sciencedirect.com/science/article/abs/pii/S0048969722074939?via%3Dihub ↩

- (November 2, 2022). E-Waste Management Rules, 2022. International Energy Agency. https://www.iea.org/policies/25027-e-waste-management-rules-2022 ↩

- Golda, A., Nair, K., Ali, M. S. & Verma, R. (n.d.). Unravelling India’s E-Waste Supply Chain: A Comprehensive Analysis and Mapping of the Key Agents Involved. https://econpapers.repec.org/paper/bdcwpaper/429.htm ↩

- (2026). Waste Management. Ministry of Environment, Forest and Climate Change, Government of India. https://moef.gov.in/waste-management ↩

- (2022). E-Waste (Management) Rules, 2022. UNEP Law and Environment Assistance Platform. https://leap.unep.org/en/countries/in/national-legislation/e-waste-management-rules-2022 ↩

- (2023). EIA Notification, 2006 with changes post 2012- 20 Mar 2023. ICNL. https://www.icnl.org/resources/library/eia-notification-2006-with-changes-post-2012-20-mar-2023 ↩

- (2022). E-Waste (Management) Rules, 2022. Government of India. https://www.scconline.com/blog/post/2022/11/03/government-notifies-e-waste-management-rules-2022/ ↩

- (n.d.). Environmental Labs. Ministry of Environment, Forest and Climate Change, Government of India. https://moef.gov.in/environmental-labs ↩

- (2022). E-Waste (Management) Rules, 2022. International Energy Agency. https://www.iea.org/policies/25027-e-waste-management-rules-2022 ↩

- GreenSutra®. (2026). E-Waste EPR Explained 2026 | Targets, Certificate Prices and the CPCB Portal. GreenSutra. https://greensutra.in/news/e-waste-epr-explained-2026/ ↩

- (2022). E-Waste Management Rules, 2022. International Energy Agency. https://www.iea.org/policies/25027-e-waste-management-rules-2022 ↩

- (2022). Implementation Guidelines for Recyclers. Central Pollution Control Board. https://cpcb.nic.in/uploads/Projects/E-Waste/Guidelines_Environmentally_Sound_Recycling_E-Waste.pdf ↩

- Huang, T., Zhu, J., Huang, X., Ruan, J. & Xu, Z. (2022). Assessment of precious metals positioning in waste printed circuit boards and the economic benefits of recycling. Waste Management 139, pp. 105-115. https://doi.org/10.1016/j.wasman.2021.12.030 ↩

- (2023). A review on recovery processes of metals from E-waste: A green perspective. Science of The Total Environment 859. https://doi.org/10.1016/j.scitotenv.2022.160391 ↩

- Panchal, R., Singh, A. & Diwan, H. (2021). Economic potential of recycling e-waste in India and its impact on import of materials. Resources 74. https://doi.org/10.1016/j.resourpol.2021.102264 ↩

- Wath, S. B., Gajghate, S. V. & Deshmukh, S. R. (2013). Electronic waste – an emerging threat to the environment of urban India. Journal of Environmental Health Science and Engineering 11(1), pp. 1-11. https://doi.org/10.1186/2052-336X-11-1-1 ↩